How the CHIPS Act Affects Tax Credits

Authored by: Brett Leibfried — Partner, CPA | Date Published: January 27, 2026

Understanding the Advanced Manufacturing Investment Credit and What It Means for Your Business

When dealership lots sat empty after the pandemic, manufacturers were scratching their heads. Factories were still capable of building vehicles, so what was the problem? They couldn’t get their hands on the tiny semiconductor chips that power everything from entertainment systems to engine controls.

America had become dangerously dependent on overseas chip production, and so the CHIPS Act entered the industry. For eligible U.S.-based companies, this tax credit became the solution to national competitiveness. Let this blog be your guide to understanding how manufacturing has been affected.

Featured Topics:

What is the CHIPS Act?

Signed into law in August 2022, the “Creating Helpful Incentives to Produce Semiconductors” (CHIPS) Act intended to bring microchip manufacturing back to the United States after decades of offshoring the technology.

But what does this have to do with taxes?

Enter the Advanced Manufacturing Investment Credit. This powerful credit was designed to aid American semiconductor manufacturing. Think of the AMIC as the government’s way of saying, “We’ll help you pay the bill if you build it here.”

Starting in 2026, the credit rate jumped from 25% to 35% for property focused on semiconductor production. The best part is that it’s not a loan you have to pay back. It simply returns to your bottom line.

Here’s what else makes the CHIPS Act so appealing: The credit comes with elective pay, also known as “direct pay.” Instead of waiting to apply the credit to future bills, eligible taxpayers can elect to receive an actual check from the IRS. This means immediate cash in hand for partnerships, S corporations, or companies that lack tax liability.

Claiming this credit requires serious proactive effort, but the key question becomes, “Who actually qualifies for this benefit?”

What are the Qualifications for the AMIC Credit?

The beauty of the credit is that it recognizes the entire industry required to make semiconductors domestically. You don’t have to be Intel or Samsung to benefit; it all comes down to meeting certain eligibility requirements.

Let’s look at who qualifies:

- Semiconductor & Equipment Manufacturers

- Real Estate Developers and Infrastructure Investors

- Pass-Through Entities

Whether you’re running a manufacturer or an expanding equipment company, the next step is to understand which properties qualify. The regulations provide specific guidance on what constitutes “qualified property.”

Under Section 48D, an asset must meet all the following criteria:

- Tangible Property: Tangible personal property or structural components.

- Depreciable: Eligible for depreciation or amortization under normal tax rules.

- Integral to Operations: Directly used in or essential to the manufacturing operation.

- Original Use or Construction: Either constructed by or first used by the taxpayer.

- Part of Facility: Physically located at the facility or on contiguous land.

Unlike many investment credits, this refund includes all the structural components of the operation. However, it is still important to check if your specific operations meet the qualifications. If you’re unsure, consider partnering with our manufacturing advisors to better understand your situation.

How to Turn the AMIC into Cash

Imagine you’ve just invested $100 million in a new semiconductor facility and are staring at a potential $35 million credit. Qualifying for the credit is only half the battle.

Here’s how to actually claim it and convert it into savings.

Step 1: Gather Documentation

With detailed documentation of all qualified investments and related expenses, you can accurately register for the credit. This includes bills of materials, production logs, facility reports, and quality control records.

Step 2: Complete Pre-Filing Registration.

Manufacturers can elect to treat the credit as a payment of tax equal to the amount of the credit, receiving a payment instead of claiming the credit. This is called the direct pay option.

To do so, the taxpayer or entity must:

- Pre-file Registration: Obtain a registration number using the IRA/CHIPS Pre-filing Registration Tool.

- Timely Election: File the annual return by the due date and make a valid elective payment election.

Once made, the direct pay election is irrevocable for that taxable year.

Step 3: File Required Forms with Your Tax Return

Attach the following forms to claim the credit on your annual tax for the year the qualified property is placed in service:

- Form 3468: Calculate and report your credit for any qualified investment during the taxable year.

- Form 3800: Summarizes the AMIC and all general credits and is attached to your main return.

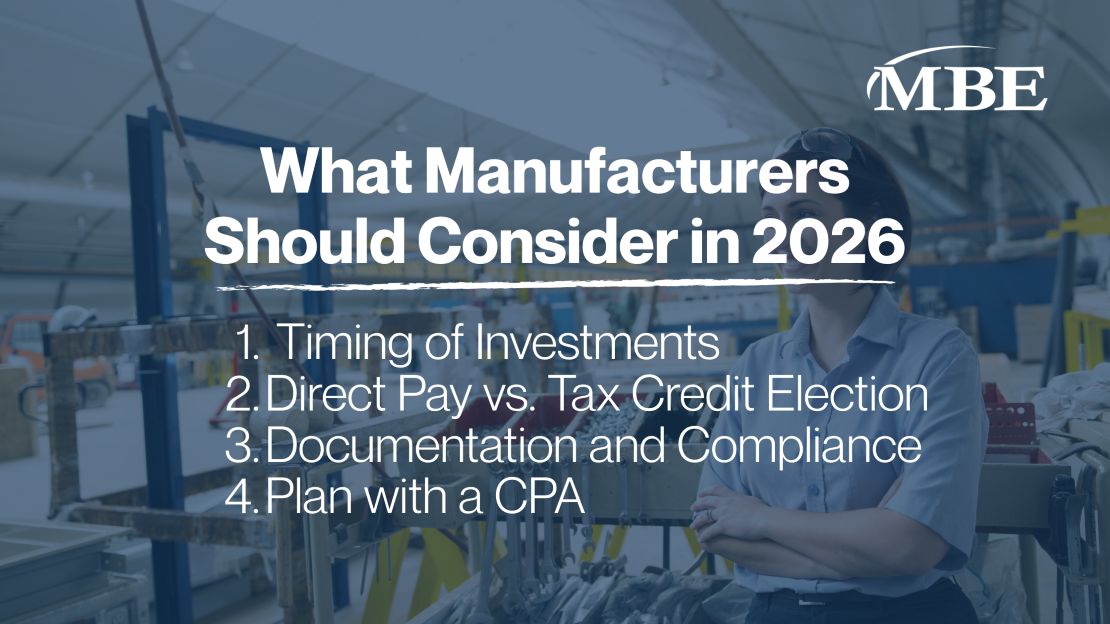

What Taxpayers Should Consider in 2026

Think about a company wanting to invest in new facilities. With the AMIC, not only would the expansion be possible, but it could also accelerate the timeline.

If you’re considering pursuing the Section 48D credit, here’s what to double-check with your advisors:

- Timing of Investments: The credit applies to property in use before January 1, 2027. Careful planning of equipment installation can make a significant difference.

- Direct Pay vs. Tax Credit Election: Highly profitable corporations with annual liability might find more value in the traditional credit to use against what they’re already paying. Pass-through entities or startups may opt for direct pay to fund expansion, R&D, or hiring.

- Documentation and Compliance: The IRS requires accurate documentation to support Section 48D claims. Beginning to record all qualified costs, allocation, and construction evidence will be beneficial.

- Plan with a CPA: Engage your CPA firm early in the planning process to establish proper documentation procedures and confirm all requirements are met before costs are incurred.

Learn more about how manufacturers can prepare for tax season.

At the end of the day, this credit really represents a commitment. The U.S. is committing to rebuilding its manufacturing capabilities. Companies are committing to building that capacity here, and only here, for at least the next decade.

The Ongoing Impact of the CHIPS Act

Step back from the technicalities for a moment and consider what’s actually happening here. The AMIC represents a massive, coordinated bet on rebuilding a critical domestic industry, and we’re already seeing the results.

For those willing to make that commitment and work with experienced advisors who understand both the technical requirements and the strategic implications, the rewards could be transformative.

You already know that credits and deductions vary depending on the industry you operate in. At MBE CPAs, our experience working across these industries helps us identify your specific tax-saving opportunities.

Are you ready to improve your manufacturing potential?