Understanding Quality of Earnings in M&A Transactions

Authored by: Ryan Weber — Partner, CPA, CVA | Date Published: February 25, 2026

When you’re preparing to sell your business, you’ll quickly discover that buyers don’t just look at your bottom line, they dig deep into how you arrived at that number. This is where a Quality of Earnings (QoE) analysis becomes critical. For sellers entering the M&A process, understanding QoE can mean the difference between a smooth transaction and a deal that falls apart during due diligence.

For sellers entering the M&A process, understanding what quality of earnings is, how a quality of earnings report works, and why buyers rely on M&A financial due diligence can mean the difference between a smooth transaction and a deal that falls apart during review.

This blog will walk you through everything you need to know about Quality of Earnings from a seller’s perspective, what it is, why it matters, and how preparing early can strengthen your position at the negotiating table.

Featured Topics:

- Why Do Buyers Focus So Heavily on Earnings?

- What Is Quality of Earnings?

- Why Does Quality of Earnings Matter When Selling a Business?

- What Do Buyers Review in a Quality of Earnings Analysis?

- What Are the Benefits of Doing a Quality of Earnings Before Due Diligence?

- When Should a Seller Get a Quality of Earnings?

- How Can Transaction Advisory Services Support a Sell-Side QoE?

- How Do Sellers Get Started with a Pre-DD Quality of Earnings?

- Final Thoughts

1. Why Do Buyers Focus So Heavily on Earnings?

In M&A, a buyer isn’t just buying your past; they are purchasing future cash flows. Their primary concern is whether your reported earnings reflect sustainable, recurring profits.

Why Adjusted EBITDA Often Isn't Enough

While you may present adjusted EBITDA as your profitability metric, buyers need more context. By doing a financial review and accounting due diligence, they may find these additional questions to ask:

- Are the adjustments legitimate and defensible?

- Will revenue continue at this pace post-acquisition?

- Are there hidden costs or risks lurking in the financials?

- How much working capital will be required to maintain operations?

Without thorough validation, even strong financial statements can raise red flags. Buyers use QoE and a due diligence report to bridge the gap between what’s on paper and what they can realistically expect to earn.

What Are Buyers Really Trying to Confirm During Diligence?

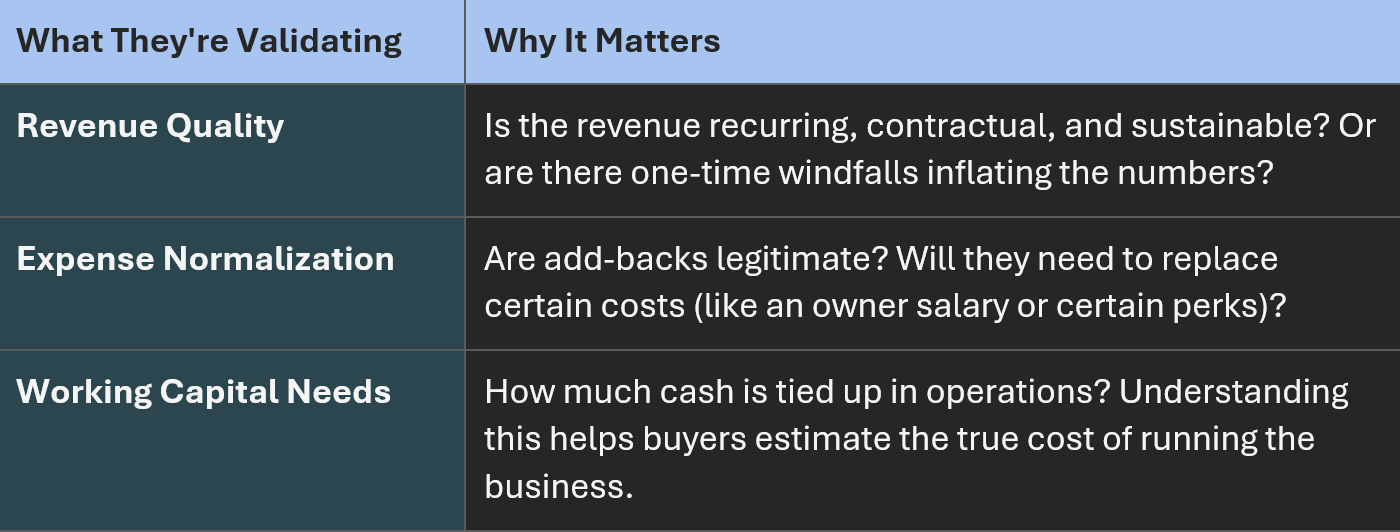

Buyers conduct Quality of Earnings reviews to validate three critical elements:

2. What Is Quality of Earnings?

In simple terms, a Quality of Earnings analysis is an independent, detailed review of your company’s financial performance. Think of it as a financial deep dive that goes beyond what’s visible in standard financial statements.

How QoE Is Defined in Simple Terms

A QoE report typically examines 2-3 years of historical financial data and provides insights into:

- The accuracy and sustainability of reported revenue

- Whether expenses are properly categorized and recurring

- The validity of EBITDA adjustments

- Customer concentration and contract strength

- Working capital trends and requirements

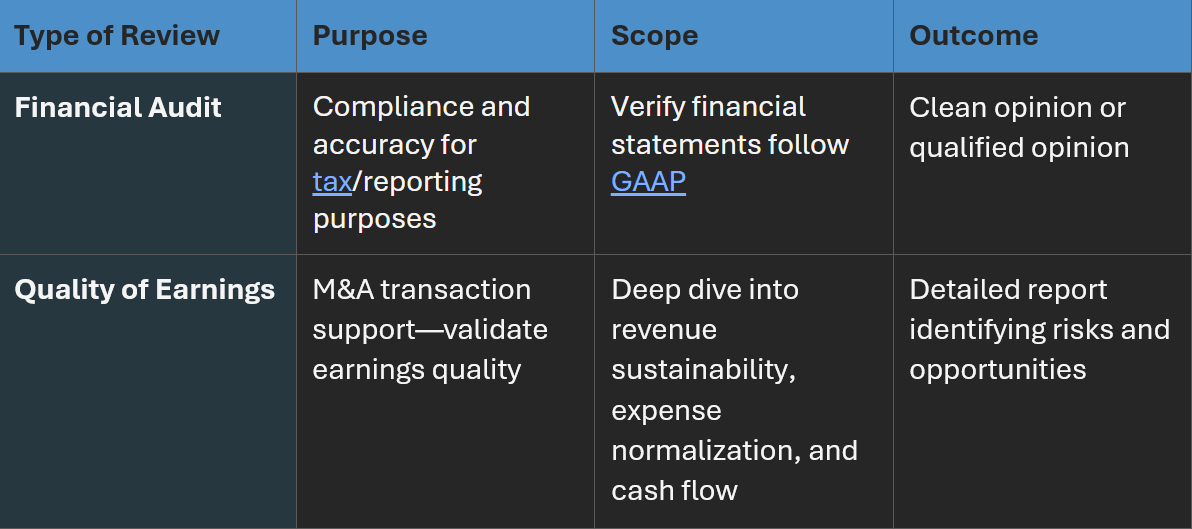

Unlike your accountant’s year-end financial statements, QoE is specifically designed for M&A transactions.

Bottom line: A QoE is purpose-built for M&A and focuses on answering the buyer’s core question—can I trust these numbers?

3. Why Does Quality of Earnings Matter When Selling a Business?

How QoE Affects Valuation and Deal Certainty

Buyers base initial offers on your financials, but their own QoE review during diligence often drives the final outcome. If they uncover issues—such as aggressive revenue recognition, unsustainable margins, or questionable add-backs—they’ll likely renegotiate. This can lead to a lower purchase price, more escrow or earnout requirements, longer timelines, or even a failed deal.

What Can Go Wrong If Sellers Skip QoE Before Going to Market

Skipping a pre-diligence QoE leaves sellers exposed. Late discoveries give buyers leverage, weaken your negotiating position, and can reveal inflated EBITDA or unrealistic expectations. These surprises often delay diligence, create deal fatigue, and increase the risk of renegotiation—or collapse. Preparing with your own QoE helps you control the narrative and negotiate from strength.

4. What Do Buyers Review in a Quality of Earnings Analysis?

Buyers use a Quality of Earnings (QoE) review to evaluate how reliable and sustainable a business’s financial performance really is.

Revenue quality: They prefer recurring, contract-based revenue over one-time sales, watch for overreliance on a few customers, check that revenue is recognized properly, and evaluate whether growth is sustainable or driven by temporary factors.

Expense normalization: Buyers review “add-backs” for owner-specific or non-recurring costs (like excess compensation, personal expenses, or one-time fees), but expect them to be reasonable, necessary, and well-documented.

Working capital and margins: They examine receivables, inventory, and payables to ensure operations are financially healthy and not being propped up by delays or excess stock. They also evaluate whether profit margins are stable or influenced by temporary advantages.

5. What Are the Benefits of Doing a Quality of Earnings Before Due Diligence?

Conducting a sell-side QoE before entering the market isn’t just good practice, it’s a strategic advantage that can significantly improve your transaction outcome.

How Pre-DD QoE Helps Sellers Identify Risks Early

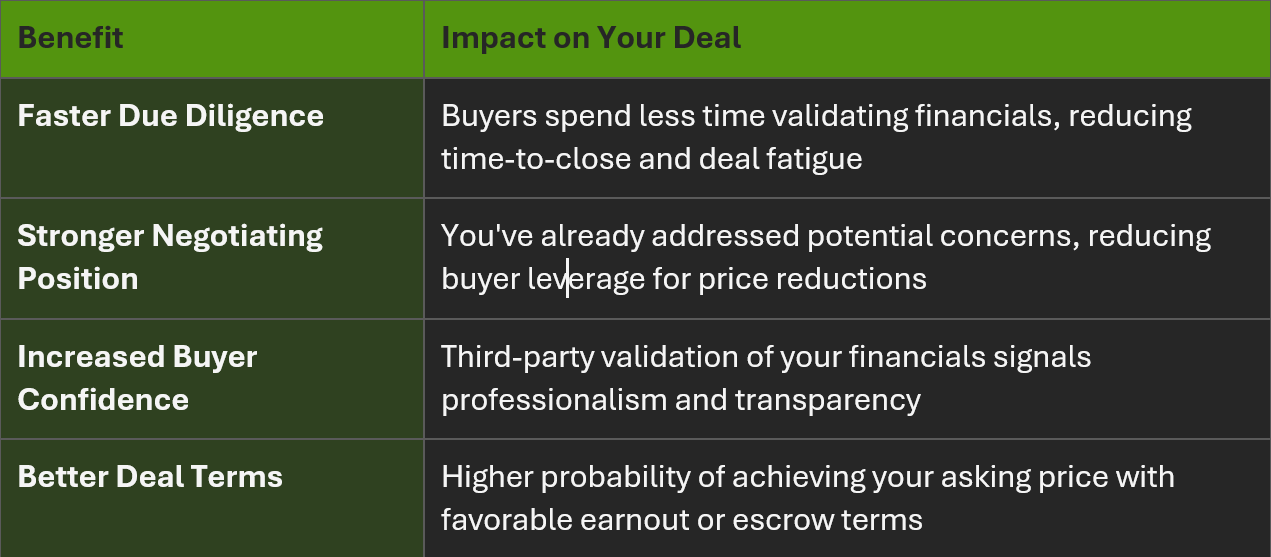

By running your own QoE analysis, you can:

- Identify and remediate accounting inconsistencies before buyers find them

- Validate your EBITDA adjustments with third-party credibility

- Understand your true normalized earnings and set realistic expectations

- Prepare compelling responses to anticipated buyer concerns

This proactive approach means you control the narrative rather than reacting defensively during buyer due diligence.

Why Proactive QoE Can Improve Negotiations and Timelines

When you provide a sell-side QoE report upfront:

6. When Should a Seller Get a Quality of Earnings?

Ideal Timing Relative to the Sale Process

The best time to complete a sell-side QoE is 6–12 months before going to market, giving you time to fix issues, improve financial reporting, and present a credible investment story. If you’re already in buyer discussions, a full pre-deal QoE may be late—but a limited review can still help you prepare for questions and support your position.

Signs a Business Is Ready (or Not) for QoE

A business is typically ready if it has 2–3 years of consistent financials, reasonably organized accounting, and plans to sell within 12–18 months. It may not be ready if financial records need major cleanup, operations are changing significantly, or ownership is not yet serious about selling.

7. How Can Transaction Advisory Services Support a Sell-Side QoE?

What Sellers Should Expect from a Sell-Side Analysis

A sell-side QoE reviews revenue quality, expenses (including add-backs), working capital needs, and normalized EBITDA, while identifying potential risks buyers may raise. The result is a detailed report that supports your financial story and can be shared with prospective buyers.

How Advisors Work with Management and Investment Bankers

Transaction advisors collaborate with management to gather data and understand operations, align with investment bankers on deal positioning, and coordinate with legal and tax teams on structure and disclosures—ensuring the QoE supports the overall transaction strategy.

8. How Do Sellers Get Started with a Pre-DD Quality of Earnings?

What Information Is Typically Required

To complete a QoE, advisors typically request 2–3 years of financial statements, general ledger and trial balance details, customer and vendor records, tax returns, and documentation supporting EBITDA add-backs. While this may seem extensive, most businesses with basic bookkeeping already have much of this information, and advisors help organize the rest.

Final Thoughts

Selling a business is one of the most significant financial decisions you’ll ever make. The Quality of Earnings process, whether you proactively conduct it or the buyer conducts it during due diligence, will play a central role in determining your transaction outcome.

By understanding what buyers look for, addressing potential issues early, and presenting your financials with third-party validation, you position yourself to negotiate from a position of strength, close faster, and maximize your sale price.