What Is a Trust in Estate Planning?

Authored by: Greg Patel — Partner, CPA | Date Published: June 01, 2026

If you’ve ever nodded along as an estate planning attorney or accountant mentioned a “trust,” only to wonder what it really means, you’re not alone. Many families hear the term repeatedly before truly understanding what’s being offered.

Truthfully, trusts aren’t complicated in concept. They’re powerful, flexible tools that have been used for centuries to protect wealth, care for loved ones, and pass assets across generations. Once you understand the basics, you’ll start to see why so many families, not just the ultra-wealthy, find value in using them.

Let’s break it down together.

Why Would Someone Need a Trust?

At its core, a trust is a legal arrangement where one person or institution (the trustee) holds and manages assets for the benefit of another individual or group (the beneficiaries).

Imagine leaving town for an extended period and relying on someone you trust to watch over your home while you’re away. You hand over the keys, provide instructions, and explain exactly what you want done, trusting your friend to carry out your wishes. A trust works much the same way, except the assets involved might be investment accounts, real estate, life insurance policies, business interests, or virtually anything else you own.

The key distinction between a trust and simply giving something to someone is control. With a trust, you set the rules, the assets are managed according to your instructions, for the people you choose, and for as long as you determine. This level of control is what makes trusts so valuable in estate planning.

What is the Difference Between a Grantor, a Trustee, and a Beneficiary?

Every trust has three main roles, and it’s common for one person to fill more than one.

The Grantor

This is the person who establishes the trust and transfers assets into it. This role defines the terms, including how assets are managed and distributed.

The Trustee

The trustee is the person or institution responsible for managing the trust assets according to your instructions. This can be you, a family member, or a professional.

The Beneficiary

Beneficiaries are the people or entities who benefit from the trust. Receiving income, distributions, or eventually the trust assets themselves.

For example, in a typical living trust, a married couple might be both the trustees and the beneficiaries during their lifetimes. They would name a successor trustee to take over management if they become incapacitated or pass away. This structure is intentionally flexible.

How Does a Trust Actually Work?

When you establish a trust, you transfer ownership of specific assets into it. Legally, the trust becomes the owner. Not you personally, and not your estate. The trustee then manages those assets according to the document you created, which covers:

- Who the beneficiaries are and what they’re entitled to receive

- When and how distributions are made (age milestones, life events, discretion of the trustee)

- Who manages the trust if the original trustee is unable to continue

- What happens to the remaining assets when the trust ends

- Any special conditions or protections (e.g., protecting a beneficiary from creditors, or providing for a child with special needs)

Since the trust is a separate legal entity, assets held in a properly funded trust usually bypass the public and time-consuming court process known as probate. Instead, they pass directly to your beneficiaries. Privately, efficiently, and as you intended.

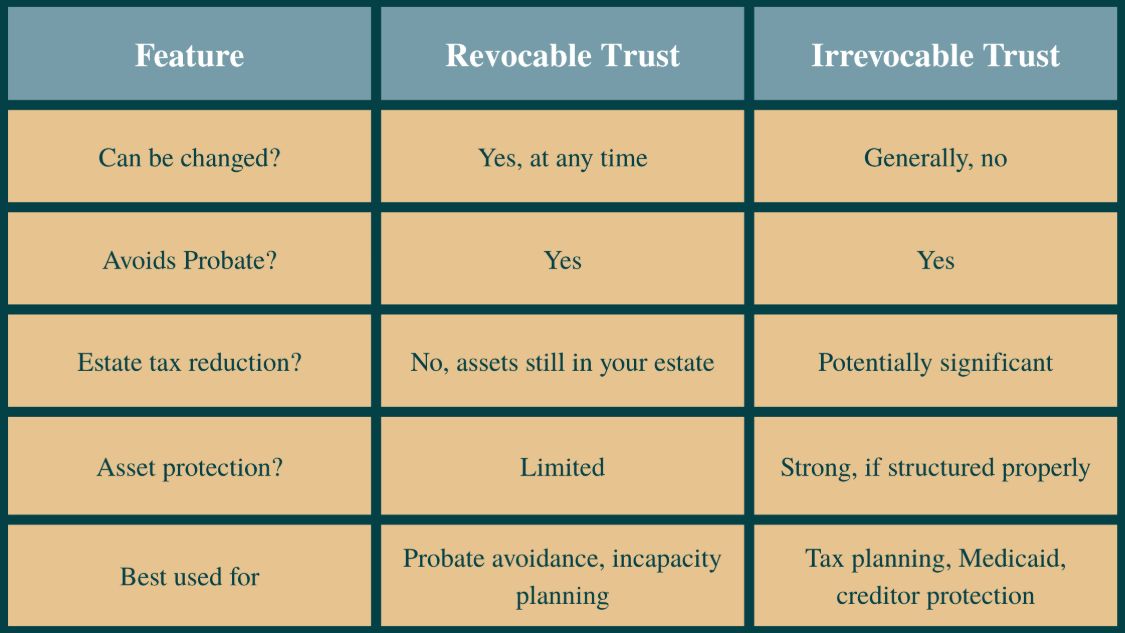

Should I Get a Revocable or an Irrevocable Trust?

These are two of the most common trust structures, and the right choice depends on your priorities. The key difference comes down to control and flexibility versus long-term planning benefits. A revocable trust allows for ongoing control and changes during your lifetime, while an irrevocable trust involves giving up that control in exchange for potential advantages related to taxes, asset protection, and legacy planning. Understanding how each approach works will help you evaluate which structure best fits your situation.

Revocable Living Trust

This is the most common type of trust for individuals and families. You establish and fund it with your assets, retaining full control during your lifetime. You can modify, amend, or revoke it at any time. Upon your death, it becomes irrevocable, and your successor trustee carries out your instructions. Key benefits include avoiding probate, maintaining privacy, and allowing for easy management of your assets if you become incapacitated.

Irrevocable Trust

Once created and funded, an irrevocable trust cannot be easily changed or undone. This restriction is intentional. In exchange for giving up direct control over the assets, you gain powerful benefits. Irrevocable trusts can help reduce estate taxes, protect assets from creditors, qualify for Medicaid, or facilitate substantial gifts to heirs or charities. Because of the loss of control, these trusts are typically reserved for specific, well-planned goals.

Why Do Families Use Trusts?

There’s no single answer. Different families use trusts for different reasons. Here are the most common ones we see:

Avoiding Probate

Probate is the court-supervised process of distributing your assets after death. It’s public (anyone can look up the records), it takes time (often 9–18 months or longer), and it can be costly. Assets held in a trust avoid probate entirely, sparing your family time, expense, and additional stress during an already difficult period.

Protecting Minor Children or Vulnerable Beneficiaries

If something happened to you tomorrow, would you want an 18-year-old to inherit a large sum all at once? Most parents wouldn’t. With a trust, you can stagger distributions. Perhaps one portion at age 25, another at 30, or tie them to milestones such as graduating college or maintaining employment. For a child with special needs, a specially designed trust can provide ongoing support without jeopardizing their eligibility for government benefits.

Reducing Estate Taxes

For larger estates, federal (and sometimes state) estate taxes can claim a significant share. Certain irrevocable trusts are specifically designed to move assets out of your taxable estate, allowing you to pass more wealth to your children and grandchildren instead of the IRS.

Privacy

A will becomes a public record when probated, but a trust remains private. For families who value confidentiality and wish to avoid disputes or outside scrutiny, this is a major advantage.

Planning for Incapacity

A trust doesn’t just plan for death. If you become unable to manage your own affairs due to illness or injury, a successor trustee can step in immediately to manage your assets without court intervention. It’s one of the most practical and often overlooked benefits of a well-designed trust.

Do I Really Need a Trust for My Estate?

It would be easy to read all of this and assume that everyone needs a trust. In reality, for many families, a simple will combined with beneficiary designations is enough. But for those with minor children, blended families, closely held businesses, significant assets, or a loved one with special needs, a trust can be essential.

The right answer depends on your specific situation. The size and nature of your assets, your family dynamics, your wishes for the future, and the current tax environment. That’s the kind of conversation a good estate planning advisor can have with you.

If you’ve been putting this off, don’t wait. Thoughtful planning is one of the greatest gifts you can give your family.

Ready to talk about your family’s plan? Contact MBE CPAs to explore whether a trust is right for you and which type would best protect your goals. We work closely with your financial planning providers and attorney to create a seamless, stress-free process.