Common Expenses That Reduce Your Final Inheritance

Authored by: Greg Patel — Partner, CPA | Date Published: June 12, 2026

A family spends decades building wealth carefully, thoughtfully, and with their descendants in mind. They’d been promised a full inheritance, but instead received a number chipped away by taxes and obligations nobody warned them about.

Many families assume estate taxes are the primary cost standing between their loved ones’ full inheritance. The reality is that several other fees can substantially erode the deal. Understanding the full range of complex costs is foundational, or you’ll quietly lose value in the transfer process.

Let’s walk through each of them.

Are Estate Taxes the Only Taxes that Apply to Inheritances?

This is where the misconception usually starts. Most people hear “estate tax” and assume if their estate falls below the threshold, they’re in the clear. Technically, that’s true.

Estate taxes apply only to those above specific federal and state thresholds. If below the applicable exemption (historically in the millions), they owe no federal tax.

However, that exemption is not permanent. It’s subject to legislative change, and its scheduled sunset provisions mean that a family comfortably under the threshold today may not be tomorrow.

Even when it falls comfortably below the threshold, other tax obligations can still affect what beneficiaries receive. The absence of an estate tax bill does not mean an inheritance arrives tax-free.

Let’s break down what they’re actually facing: income, capital gains, and state-level taxes.

What is an Inheritance Tax and Who Pays It?

It’s important to distinguish between two concepts that are frequently confused. The mix-up is understandable, but this distinction matters:

- Estate tax: levied on the estate itself before assets are distributed to heirs.

- Inheritance tax: paid by the beneficiary after receiving assets, and it is imposed at the state level, not the federal level.

What does this look like in real life?

A family in a state that imposes inheritance taxes passes down an investment portfolio to a niece. She wasn’t a direct descendant, so she may be taxed at a substantially higher rate than a sibling or child would have been.

Rates vary widely based on the descendant’s relationship with the deceased. Surviving spouses are typically exempt, and direct descendants often face lower rates. But distant relatives or unrelated beneficiaries may face substantially higher rates.

For families with assets or inheritors spread across multiple states, this can quickly get complicated. The rules of the state where the asset is located and where the heir lives both come into play, so careful mapping of each jurisdiction’s tax rules is important.

Do Beneficiaries Pay Income Tax on Inherited Assets?

Inherited assets do not always arrive tax-free. There are several common scenarios where heirs find themselves with real tax obligations.

Let’s take a look at these scenarios:

- Retirement Accounts: You can’t inherit a large IRA and just let it grow. Non-spouse beneficiaries are required to fully distribute an inherited retirement account within ten years, and each withdrawal is taxed as ordinary income.

- Income-Producing Assets: Real estate holdings, dividend-paying investments, and business interests generate ongoing income. This doesn’t pause because they changed hands. Rent, dividends, and business profits are taxable to the heir in the year they are received.

- Installment Payments and Deferred Compensation: An inheritance that includes installment sale receivables, seller-financed arrangements, or deferred compensation plans may carry taxable income that surfaces over time. Each payment received by the heir includes an income component subject to tax.

These are scenarios nobody loves, but the rules can’t be ignored. Withdrawals are stacked on top of your salary, and suddenly your tax bracket is higher.

Let’s talk about something that actually works in heirs’ favor

What is Capital Gains Tax on Inherited Assets?

Have you heard of the step-up in basis?

This is one of the most valuable provisions. When an asset is inherited, its tax basis is reset to its fair market value at the date of death. That means appreciation that accumulated during the original owner’s lifetime is never subject to capital gains tax.

That said, there are still situations where capital gains taxes applies:

- Post-inheritance appreciation: If heirs sell an inherited asset after it has been further appreciated, gains above the step-up basis are taxable.

- Assets without a full step-up: Assets held in irrevocable trusts or transferred during the owner’s lifetime may not receive a full basis adjustment.

- Depreciation recapture: Real estate and assets that have depreciated over time may be subject to recapture tax even when the step-up in basis applies.

Understanding which assets will and won’t receive a step-up is the kind of detail that separates good from great estate planning.

What Administrative Costs Can Affect an Estate?

Beyond taxes, there’s an entire category of costs that directly reduce what descendants receive, and many families never think about them.

For fortunes involving business interests, real property, or complex ownership structures, these costs deserve careful attention:

- Probate Fees

- Legal Fees

- Accounting Fees

- Executor Compensation

- Asset Appraisal Costs

- Ongoing Asset Management

Between appraisals, legal work, accounting, and probate, the cost of settling the inheritance starts to add up. None of these costs are avoidable entirely, but with advance planning, many of them can be significantly reduced.

Can State Taxes Impact Inheritance?

The short answer is yes, and can be the most complex part of the picture,

While federal law sets the framework for estate and income taxes, states have independent authority to layer in their own rules. And many do.

Some states impose taxes with exemption thresholds well below the federal level, meaning properties that owe nothing federally may still face a meaningful state estate tax bill. Others impose inheritance taxes on beneficiaries directly. Retirement account distributions or income generated by inherited assets can be taxed at the state level.

With assets or heirs residing in multiple states, the interplay of these regimes can be unexpected. A proactive, state-by-state tax analysis should be part of every comprehensive estate plan, not an afterthought.

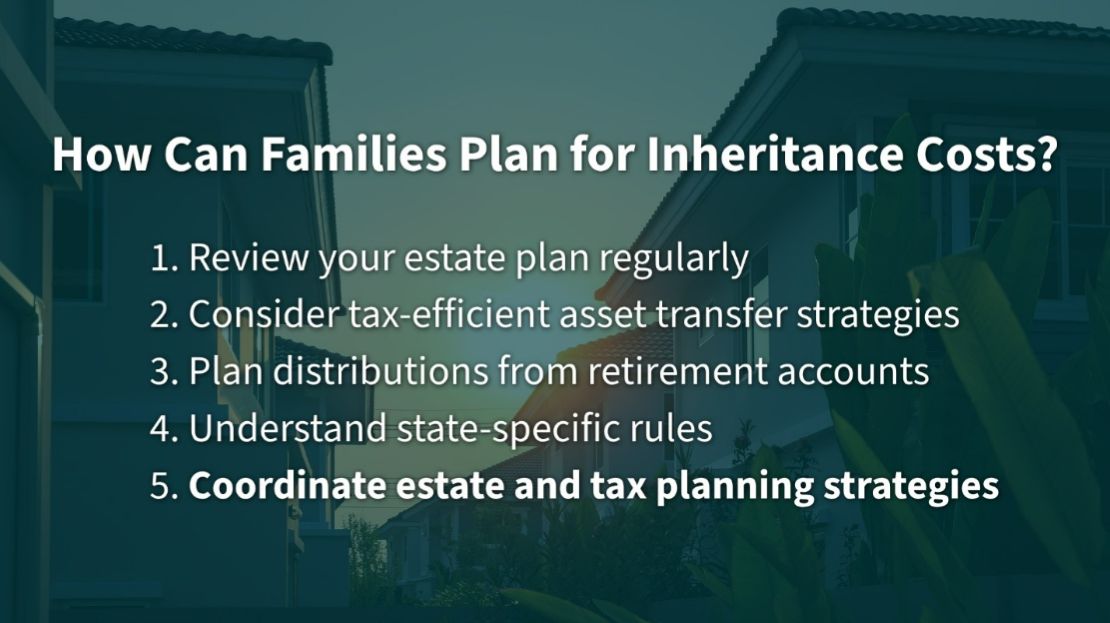

How Can Families Plan for These Costs?

The most effective way to protect your legacy is to plan early, comprehensively, and adapt as tax laws evolve.

Here’s where to start:

- Review your estate plan regularly

- Consider tax-efficient asset transfer strategies

- Plan distributions from retirement accounts

- Understand state-specific rules

- Coordinate estate and tax planning strategies

This level of planning is far more than a single tax line item. Do you have the right planning in place to mitigate these costs?

Our team can help you with this. At MBE CPAs, we help high-net-worth families develop coordinated strategies that protect what you’ve built. We want your family to receive the greatest possible benefits just as much as you do.

If it’s been a while since you’ve reviewed your estate plan, or if your situation has changed, we’d welcome the opportunity to take a closer look.