Should You Move to Save Taxes?

Authored by: Diane Payne — Partner, CFP®, EA | Date Published: July 06, 2026

Remote work and increased financial mobility have given more people the freedom to choose where they live, and many are using that freedom to leave high-tax states behind. The desire to optimize net income is driving a growing number of individuals and families to relocate to low- or no-income-tax states. This has sparked a rise in tax-centric financial planning discussions.

So, will moving actually reduce your tax burden? The answer depends on several financial and legal factors and understanding them before you make a decision could save you from a costly surprise down the road.

Why Are People Moving to Lower-Tax States?

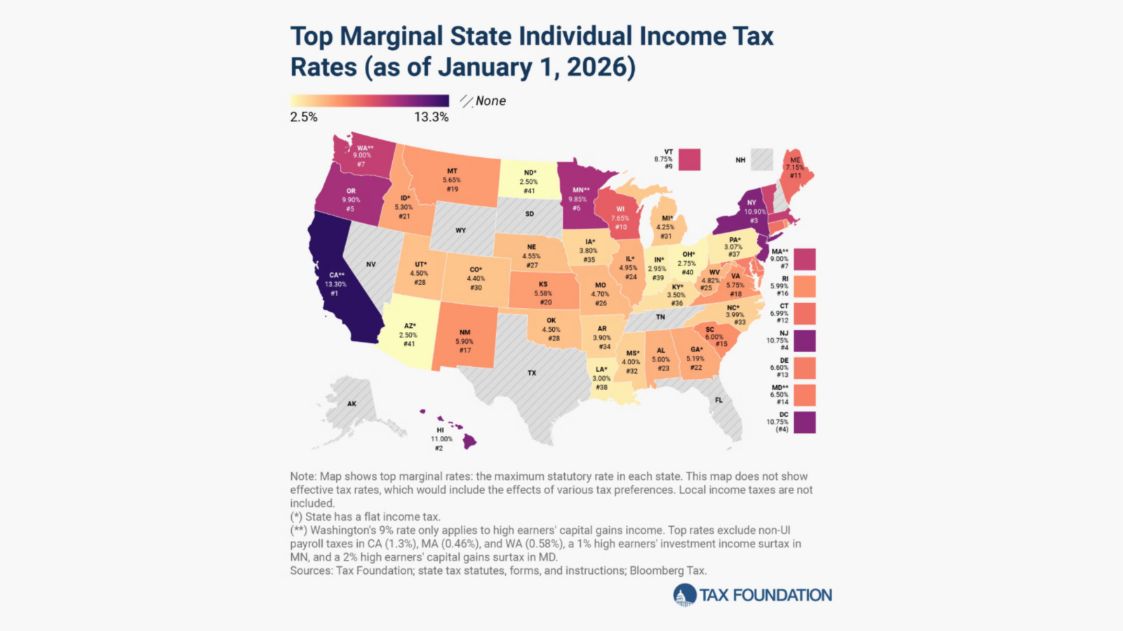

Nine states currently impose no individual income tax, which include Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington, and Wyoming. For someone earning a high income, the annual difference in state tax liability between a high-tax state and a no-income-tax state can reach tens of thousands of dollars. That kind of number has a way of making people take a closer look at where they live.

Remote work has made that closer look more actionable, removing the geographic anchor that once tied households to a specific location. Combined with the growing number of people approaching retirement, running businesses, or holding assets that have appreciated significantly, it’s easy to see why more people are considering this decision.

Taxes are one part of this decision, though. The cost of living, proximity to family, access to healthcare, and quality of life all belong in the equation.

Does Moving to Another State Reduce Your Taxes?

Here’s where many people are surprised. Moving to a no-income-tax state eliminates one line item from your tax picture, but understanding the full picture requires looking at several other categories that may offset what you expect to save.

States fund their budgets one way or another, and states without income taxes often make up that revenue through higher property taxes, higher sales taxes, or other types of taxes. Before concluding that a move will benefit you financially, you need to look at:

- Property taxes, which vary dramatically and can run significantly higher in states without income tax.

- Sales taxes, which affect everyday spending and add up annually.

- Estate or inheritance taxes, which matter enormously for individuals with significant assets and long-term planning goals.

State tax structures vary widely enough that two people with the same income, but different financial profiles, can get very different outcomes from the same move. You need to examine each tax category together to understand the full impact.

What Taxes Should You Compare Before You Move?

Comparing every major tax category gives you the clearest view of what you’re moving into and leaving behind.

State Income Tax

Compare rates, brackets, and how different types of income are treated. On a $200,000 income, moving from a state with a 10% top marginal rate to one with no income tax could mean $14,000 to $20,000 added back to your annual take-home.

Property Taxes

States such as New Hampshire and Texas carry some of the highest property tax rates in the country. A higher property tax bill can quickly offset income tax savings, particularly if you own real estate of meaningful value.

Sales and Excise Taxes

The difference between a state with no sales tax and one with a rate above 9% adds up significantly over the course of a year. This includes purchases such as groceries, home goods, and clothing, categories that affect most households regardless of income level.

Estate and Inheritance Taxes

Federal estate taxes have high exemption thresholds, but certain states impose their own with much lower limits. Per the IRS estate and gift tax guidance, a small number of states also charge a separate inheritance tax on recipients. Choosing a state with favorable treatment here can make a lasting difference for your beneficiaries.

How Do You Legally Establish Residency in a New State?

Moving to a new state is not simply a matter of updating your mailing address. Your legal home for tax purposes is called your domicile, the permanent place you intend to return to indefinitely. You can only have one domicile at a time; it doesn’t change automatically when you move, and it determines which state has the right to tax your income. States use objective, fact-based factors to evaluate domicile, and the standard is higher than most expect. Typical indicators include:

- The number of days you physically spend in each state throughout the year.

- Where you hold your driver’s license and vehicle registration.

- Where you are registered to vote.

- Where your primary home, major possessions, and financial accounts are located.

- Where your family ties and professional relationships are centered.

Filing a certificate of domicile or registering to vote in a new location alone isn’t enough. States look at the totality of where your life is centered, so documentation needs to reflect real, sustained changes.

Can Your Former State Still Tax You After You Move?

Even after you’ve relocated, your former state may still have a claim on income tied to that state. States can tax nonresidents on income sourced within their borders, meaning that payments connected to work performed there don’t automatically become tax-free once you move. Income from equity compensation plans, for example, is often taxed based on where you lived when the underlying shares become available to you, or the options were granted, not where you live when you receive the payment. Other income that may follow includes:

- Wages earned for work physically performed in the former state.

- Rental income from property that remains in the former state.

- Business income, deferred compensation, or installment sale payments tied to work or activity that took place in the former state.

Nonresident filing requirements vary widely by state, and states with aggressive residency enforcement closely review former high-income residents, especially those who maintain ties such as a second property or ongoing business interests.

When Does Relocating for Tax Savings Make the Most Sense

Timing matters. A move planned well in advance of a major financial event can result in meaningful tax reduction, while one made too late may yield little benefit. Relocating tends to have the greatest impact when it happens:

- Before selling a business, keeping in mind that where the business is located can also factor into how proceeds are taxed.

- Before a large investment payout or equity distribution tied to a company exit.

- Prior to realizing large capital gains on investments or appreciated real estate.

- Before entering retirement, particularly if you plan to draw significant income from retirement accounts.

- During a transition to full-time remote work, when your income is no longer tied to a specific location.

What Should You Do Before Relocating for Tax Reasons

This decision rewards preparation. Taking the right steps before your move, rather than scrambling to sort things out afterward, gives you the best chance of getting the outcome you’re hoping for. Here’s where to start:

- Model the total tax picture across both states. Compare income taxes, property taxes, sales taxes, and estate tax implications side by side.

- Evaluate cost of living differences. Housing, insurance, utilities, and other expenses vary widely between states.

- Understand the residency rules in both states. Know how many days you can spend in your former state and what documentation you’ll need.

- Review income that may still be sourced from your old state. Deferred compensation, rental income, and installment payments may still be taxable after you move.

- Consult a tax advisor before the move, not after. Early guidance gives you time to plan the transition and avoid unexpected tax bills.

Is Moving States the Right Move for Your Finances

Relocating for tax savings can be a sound financial decision when it’s approached with all relevant factors considered and with the right planning in place. The answer is still different for every person, and it depends on your complete tax profile, your life circumstances, and how thoroughly you’re prepared to establish legal residency in your new home.

At MBE CPAs, we work alongside individuals making these exact decisions, and we believe you deserve guidance that reflects your situation and your long-term goals. If you’re considering a move and want to understand what it would truly mean for your finances, we’re here to work through it with you.