What OBBBA Means for Your Farm

Authored by: Kevin Block — Partner, CPA | Date Published: September 24, 2025

The fields you farm today were likely worked on by your grandparents, and maybe even their grandparents before them. This connection to the land and to your family’s history is what makes agriculture more than just a business; it’s a legacy. But with each new generation comes a new set of challenges, and in our lifetime, few have been as persistent as the demands of tax law. We’ve watched as legislation has shifted, sometimes for the better, sometimes creating new hurdles.

The recently passed “One Big Beautiful Bill Act” (OBBBA) introduces a range of changes that may impact how farm businesses manage their finances. The law’s provisions, phased in over several years, include adjustments to investment, succession, and tax planning for agricultural operations.

At MBE CPAs, we believe knowledge is power, and understanding these new rules can help you adapt your tax strategy to changing circumstances.

Featured Topics:

Why Does OBBBA Matter to Your Operation?

The agriculture industry faces unique financial challenges that most businesses never encounter. Unpredictable weather, fluctuating commodity prices, and market shifts all contribute to significant income volatility. The One Big Beautiful Bill includes measures designed to address these uncertainties and help you manage through the ups and downs.

More than 850,000 farms and ranches nationwide have a lower tax bill under the Section 199A Qualified Business Income (QBI) deduction provision, and this legislation makes that benefit permanent. This change may impact the bottom line for many farms and ranches, potentially allowing for different decisions about reinvesting in the operation or setting aside funds for future needs.

What Provisions Exist for Income and Weather-Related Events?

Farm Income Averaging

A farm’s long-term financial health depends on how it manages high-income years. The OBBBA continues the existing approach to farm income averaging, which allows eligible taxpayers to spread income over several years and prevent a bumper crop year from pushing them into a higher tax bracket. This provision:

- Provides a three-year averaging window to reduce tax spikes during bumper crop years.

- Remains available to sole proprietors, partners, and shareholders of S corporations engaged in farming.

- Requires that only farm income from the current year be used, with no income needed in base years.

- Changes the way taxes are calculated following profitable seasons.

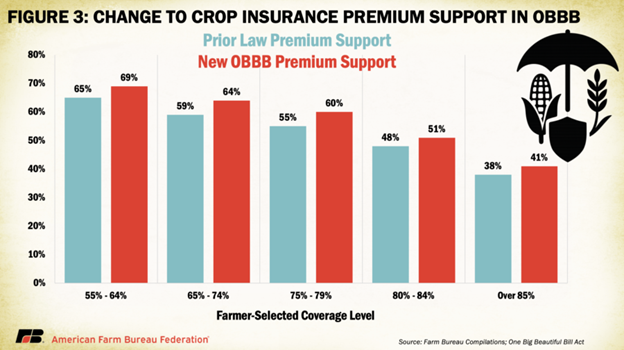

Disaster and Crop Insurance Payments

When natural disasters, such as droughts, floods, or storms, occur, the OBBBA introduces new guidelines for handling related insurance and disaster relief payments. Because crop insurance and disaster relief payments often arrive as lump sums, they can create sudden income spikes in years when your production is already low. The OBBBA’s Section 136 now provides more flexibility for managing this income.

The key features of this provision are:

- Offers a deferral election for crop insurance and disaster payments.

- Requires meeting the 50% test, which means more than half of your normal crop income would have been reported the following year.

- Provides flexibility for managing taxable income during difficult years.

Weather-Related Livestock Sales

Sometimes survival means making hard choices about your herd. Whether it’s drought forcing early culling or flooding, these situations create both operational and tax challenges. The OBBBA recognizes this reality with a special provision for livestock sales.

Here’s how it works:

- Provides a four-year replacement period for livestock sold due to drought, flood, or other weather conditions.

- Allows gain deferral when livestock is replaced within the specified timeframe.

- Enables the IRS to grant extensions beyond four years in certain circumstances.

This provision provides a mechanism to defer gains, which may assist in the process of rebuilding your herd after a forced sale.

How Can You Invest in Your Future with Equipment and Land Improvements?

Depreciation and Expensing

Purchasing new equipment often involves significant upfront costs for farms. Under OBBBA, the Section 179 expensing limit increases to $2.5 million for 2025, which is higher than in previous years. This allows farmers to reduce the full cost of most machinery in the same year as the equipment is placed in service.

The legislation also makes bonus depreciation a permanent feature, allowing for a 100% deduction of qualified equipment purchases made after January 19, 2025. These adjustments alter how certain purchases and investments are taxed, potentially impacting annual financial planning and the timing of equipment acquisitions.

Soil and Water Conservation Expenses

Recent changes allow for immediate deduction of qualified soil and water conservation expenses, subject to specified limits. These adjustments may influence how producers approach long-term land investments from a tax perspective. The OBBBA allows you to deduct these improvements immediately, rather than waiting years.

This provision offers the following benefits:

- Allows for an immediate deduction of qualified conservation expenses.

- Establishes a 25% limit on gross farm income, with a carry-forward provision for any excess amounts.

- Requires following plans approved by the Natural Resources Conservation Service (NRCS) or a comparable state agency.

- May influence both financial and environmental goals.

What Long-Term Planning Provisions Are Available?

Qualified Business Income (QBI) Deduction

The QBI deduction, which was previously set to expire at the end of 2025, has been made permanent starting in 2026 under recent legislation. This change removes uncertainty around the deduction’s expiration. Farming operations that qualify can continue to benefit from:

- A deduction of up to 20% on qualified business income.

- Potential tax savings without additional expenses.

- Expanded phase-in ranges for certain income limits, allowing more taxpayers to qualify.

- A new minimum deduction of $400 for active businesses with at least $1,000 in qualified business income starting in 2026.

Given that the deduction will remain available beyond 2025, farmers should consider how to include it in their ongoing tax planning.

Conservation Easements

Preserving your land for future generations while reducing the current tax burden becomes even more attractive. Many farming families struggle with the decision to place easements on their property, as they balance conservation goals with their financial needs. The OBBBA provides incentives for this important decision. The new law:

- Establishes a 100% gross income deduction limit for qualified farmers (compared to 50% for others).

- Requires deriving 50% or more of gross income from farming.

- Can eliminate the entire tax liability in the year of easement donation.

- May impact conservation goals and tax planning.

By increasing the deduction limit, this provision establishes a financial incentive for the preservation of agricultural land.

Farmland Installment Sale Options

Farm transitions often involve substantial capital gains that can create overwhelming tax bills. Whether you’re selling to the next generation or to a beginning farmer, the capital gains tax can be a major obstacle to successful farm transfers. The OBBBA provides relief through provisions that work alongside existing rules like Section 367 for certain corporate restructuring scenarios:

- Allows four equal annual installments for capital gains tax on farmland sales.

- Requires selling to qualified farmers to receive this treatment.

- Eases tax burden on sellers during farm transitions.

- Supports keeping agricultural land in production.

This provision alters the timing and structure of capital gains tax payments for certain farmland sales, potentially impacting transfer arrangements between parties.

What Are the Practical Steps for Your Farm?

Recordkeeping Requirements

Your records are your best defense when it comes to supporting deductions and complying with tax requirements. Good documentation protects you during audits and helps you identify opportunities for tax savings. The OBBBA’s new provisions require specific documentation to support your claims, such as:

- Detailed receipts and plans for all conservation expenses.

- Vehicle usage logs for farming purposes to support deductions.

- Crop insurance and disaster payment documentation.

- Equipment purchase records for Section 179 and bonus depreciation claims.

Investing time in good recordkeeping pays dividends when tax season arrives.

Planning Opportunities

The best tax strategies require coordination between timing, cash flow, and long-term goals. With the new OBBBA provisions, this is a good time to discuss opportunities like:

- Planning equipment purchase timing to maximize Section 179 and bonus depreciation benefits.

- Calculating income averaging for high-income years.

- Planning conservation projects to take advantage of additional deductions.

- Planning succession using new installment sale options.

Additional Benefits

Beyond the major provisions, several smaller benefits can add up to meaningful savings:

- Provides UNICAP exemption for farms with $26 million or less in average gross receipts.

- Offers fuel excise tax credits for on-farm fuel usage.

- Simplifies vehicle expense documentation for primarily farm-used vehicles.

- Provides flexibility for the hobby loss rule in part-time operations.

Moving Forward Together

The OBBBA introduces several new tax regulations that impact farm financial planning. It’s vital to understand how these new provisions apply to your specific operation, from logistics and product choices to equipment and personnel circumstances, to make long-term plans.

At MBE CPAs, we’re partners in your success. We understand that agriculture is more than a business; it’s a way of life that feeds communities and builds generational wealth. When applied correctly, these new tax provisions can help you invest in your operation’s future while managing challenges that arise. Whether you’re considering new equipment, planning conservation projects, or thinking about farm succession, good tax planning is an ongoing conversation that helps you make informed decisions throughout the year.

Your farm’s growth depends on how well you manage the business side of agriculture. Understanding these regulatory changes can help you make informed decisions for your operation.