How HSA Expansion Could Transform Your Benefits

Authored by: Brett Leibfried — Partner, CPA | Date Published: August 26, 2025

Taxes and spending have greatly changed following the enactment of the One Big Beautiful Bill Act (OBBBA) in 2025. Conversations surrounding OBBBA seem to focus on OBBBA’s broader tax implications, failing to represent the HSA provisions that impact employee benefits and healthcare eligibility.

How can business leaders remain proactive regarding compliance and leadership that directly impacts their employees?

Featured Topics:

What are Health Savings Accounts?

Health Savings Accounts (HSAs) are a type of personal savings account that serves as a triple-tax advantage and can pay for certain health care costs. Withdrawing from HSAs creates unique reporting considerations, as it is tax-free if used for qualified medical expenses.

Here are the expenses that qualify for HSAs:

- Deductibles

- Copayments

- Coinsurance

- Preventive care services

Insurance premiums are generally not considered qualified medical expenses.

Health Savings Accounts provide many individual benefits. Here are some points to consider:

- No federal income tax

- No expiration date on funds

- Possible use for spouse and dependents

- HSA is not affected by job changes

Providing HSAs to employees creates a bridge between personal and employer-sponsored benefits. Learn more about how HSA contributions and withdrawals work and how you can find an HSA-eligible plan.

The HSA Expansion Enacted by OBBBA

This year, OBBBA presented changes to existing plans, opportunities for new benefits, and tax-related changes that affect individuals according to their employment status. The three primary ways that HSA is expanding are as follows:

- Permanent First-Dollar Telehealth Coverage. The retroactive telehealth safe harbor will now treat plans as HDHPs without having a deductible for these services. Now, with permanent extension, digital health and telehealth providers may reassess and update their services and coverage for HDHP participants.

- Employer plan sponsors may reinstate free or low-cost coverage for telehealth services for the next plan year.

- All ACA Bronze and Catastrophic plans are considered qualifying high-deductible health plans (HDHPs). Many plans offer certain non-preventive benefits before the deductible is met, so this change introduces a great shift by automatically classifying these plans as HDHPs.

- Directing employees toward HSA-qualified marketplace plans may be an advantage as contribution limits, eligibility monitoring, and comparative effectiveness testing will be affected.

- HSA eligibility will not be affected by Direct Primary Care Enrollment. Previously, an individual would lose HSA eligibility under DPC since their care services are covered before the plan’s deductible has been met. Now that an individual remains HSA eligible, the DPC fees of up to $150 are treated as a qualified medical expense and may be paid tax-free.

- This new category of required medical expenses requires separate tracking and reporting mechanisms.

Other than these central changes, OBBBA introduced provisions that create new benefit-related opportunities. Beginning in July 2026, Trump Accounts will be available.

An Overview of Trump Accounts

A new type of individual retirement account, Trump Accounts, encourages saving for the future of your child. This account will allow annual contributions by parents and others of up to $5,000 that can be accessed when the child turns 18 years old.

There are more details to be considered about these accounts:

- Children born in the years 2025 to 2028 will be automatically enrolled and receive a one-time deposit of $1,000 from the federal government.

- Employers can contribute up to $2,500 into the Trump accounts of employees and their dependents.

- The money in the account must be invested in a qualified mutual fund.

- The account grows tax-deferred until account owners make withdrawals.

- Contributions made by parents or beneficiaries are not tax-exempt.

The main benefit of Trump Accounts is the initial $1,000 deposit by the government, and whether employers choose to contribute. However, HSAs are more generous due to their double tax exemption. Consider whether complete tax exemption or mere deferral is more beneficial for you or your employees.

From Wiley P Long, President | HSA for America

How Should Employers Plan HSA for 2026?

Following the changes from OBBBA, there are many plan terms employers should consider for the 2026 season. Having an employee-focused strategy will help businesses remain proactive amongst the necessary changes. This is a new era of workforce legislation, incorporating ways to retain employees by maximizing benefit opportunities.

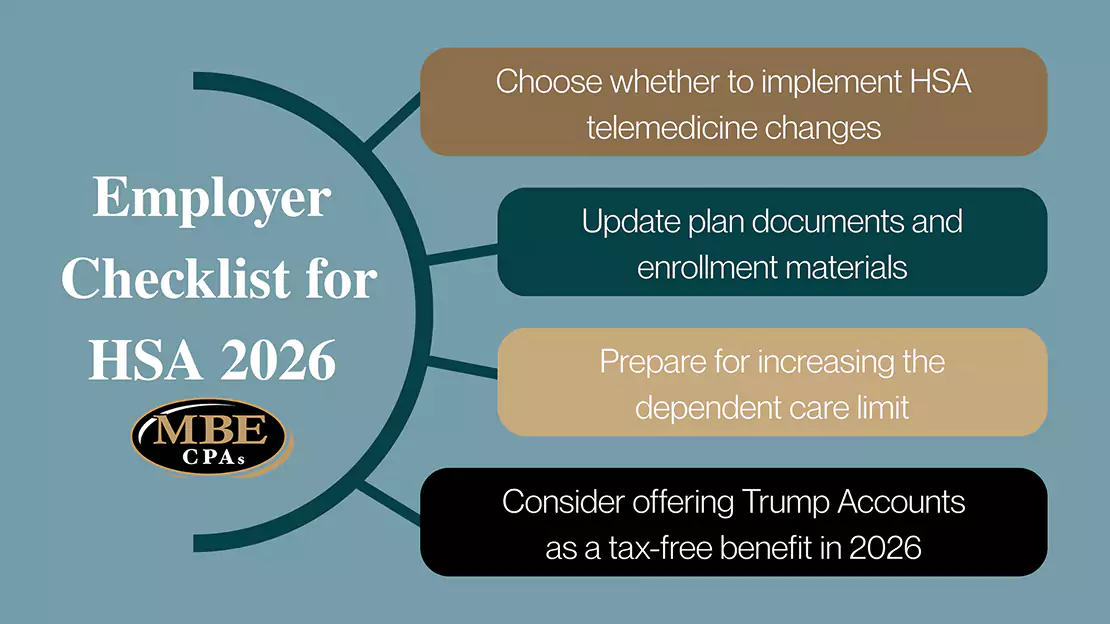

Here are the actionable measures that are relative to employee benefit plans:

- Choose whether to implement HSA telemedicine changes. The telehealth provision may necessitate adjustments to HSA eligibility determinations made earlier in 2025. Issues could arise regarding deductibles and out-of-pocket expenses already incurred.

- Update plan documents and enrollment materials. Employers should consider consulting with a professional regarding the implementation of the changes to telehealth, bronze plans, and DPC starting in 2026. Payroll and HRIS systems must be updated to accommodate expanded HSA eligibility criteria, and to prevent contribution limit violations.

- Prepare for increasing the dependent care limit. Amend plan documents and modeling testing to see the impact. Retroactive adjustments may be made for employees that are entitled to additional contributions and potential employer matching contribution adjustments.

- Consider offering Trump Accounts as a tax-free benefit in 2026. Choosing this option will require written plan documentation, compliance with nondiscrimination rules, and employee communications. Trump Accounts fall under ERISA regulations, necessitating documented investment policies and fee monitoring procedures.

As noted, employers must check if their payroll and benefits administration systems correctly reflect these changes to avoid compliance issues and potential penalties.

Even with the provisions employers should make, it is even more important to inform employees of their eligibility and updated benefits. By beginning your planning stage now, new cost-saving opportunities can be recognized that will ensure employees can fully benefit from the expanded HSA flexibility coming in 2026.

The complexity of these changes extends beyond simple policy updates. It may be beneficial for employers to meet with professionals to help steer through the intersection of federal tax law, healthcare regulations, and employment benefits.

How Should Employers Plan HSA for 2026?

Although these changes take effect in 2026, consumers can also start planning their HSA now. Here are recommendations from HSA for America:

- Maximize current HSA contributions ($4,300 individual/$8,550 family, plus $1,000 catch-up) to build funds for future DPC memberships. Consider making early contributions for tax-free growth potential.

- Treat HSA like a long-term retirement account. If possible, pay current expenses out-of-pocket to allow HSA funds to grow tax-free. This strategy can generate more wealth than traditional retirement due to triple-tax advantage.

- Keep receipts of expenses for future HSA reimbursement flexibility. There is no time limit on HSA reimbursements which creates tax-free withdrawal opportunities in retirement.

- Research DPC options. Since you’ll be able to combine DPC with HSA eligibility in 2026, search for providers’ pricing and service models.

If you’re considering changing health plans during open enrollment, factor in how the 2026 changes might affect your options. Starting research now will inform you of your decisions and allow you to take full advantage of the expanded HSA flexibility when it becomes available.

HSA Tax Strategy Planning with MBE CPAs

Enrolling your employees in the best health insurance plan is an important decision, one that will be made soon again for the 2026 season. It is essential to plan and explore practical strategies as HSA plans are becoming flexible and offering more opportunities for employers.

The risk areas that you should be aware of are as follows:

- Payroll tax compliance for employer HSA contributions

- ERISA fiduciary responsibility for investment oversight

- State insurance regulation compliance for DPC arrangements

- IRS reporting requirements for expanded HSA eligibility

Taking proactive steps means contacting MBE CPAs to maximize benefits while not compromising aspects of your business. Together, MBE can design an approach to manage the costs of adopting new healthcare plans and provide a healthy future for your employees.

Our customized tax strategies look like:

- Industry-Specific. The latest regulations and incentives relevant to your business will allow us to solve your approach for maximizing savings.

- Personalized. Our guidance is focused on your needs, goals, and priorities.

- Continued Learning Support. We provide the MBE CPAs App to send updated tax alerts and answers to tax questions to help you feel confident in your decisions.

At MBE CPAs, we provide a full range of wealth management services to help you achieve your financial objectives.

Conclusion

The One Big Beautiful Bill Act (OBBBA) has implemented the most significant expansion of HSA regulations in over a decade, creating both opportunities and challenges for employers. The complexity of these changes is much more than simple policy updates.

Given the intricate changes HSA will have on payroll, benefits, and taxes, employers should build a relationship with a qualified professional before making their 2026 decisions. With how valuable these new options will be to employees, early communication will be necessary for the upcoming open enrollment period.

Key takeaway: The expanded HSA flexibility under OBBBA requires employers to begin planning the best way to maximize employer cost savings and employee value.