Manufacturing R&D Credits Hidden in Daily Operations

Authored by: Brett Leibfried — Partner, CPA | Date Published: April 13, 2026

Your production team spent six months optimizing your injection molding cycle time. Your quality engineer developed a new testing protocol. Your maintenance crew automated part of your assembly line. Congratulations, you just conducted R&D activities worth $50,000-$150,000 in tax credits.

Here’s what most Wisconsin manufacturers miss.

Do I Have Enough R&D Expenditures to Warrant a Study?

The biggest question for manufacturers is whether you’ve been capturing the full value of what you already spend. Nearly all operations involve some level of qualifying research activity, whether that’s developing new products, improving existing processes, or engineering production solutions.

But are your Qualified Research Expenditures (QREs) substantial enough to make a formal study worthwhile?

Once your QREs approach $200,000, the return of a study begins to meaningfully outweigh the cost of conducting one. Below that threshold, the credit may still exist, just might be harder to justify.

Let’s start with the foundation of the R&D Tax Credit, Section 41 of the Internal Revenue Code. This is a credit against income tax for qualified research expenses incurred in a trade or business. For manufacturers, this is where R&D activities translate into tax savings.

It’s worth noting that R&D and R&E are related, but legally distinct under the tax code. Let’s look at why:

- R&E Expenditures: A more specific tax term, defining the how of recognizing an activity, focused on costs that qualify for tax incentives.

- R&D Expenses: The broader category of research and experimental costs that may be capitalized and amortized. This makes R&D more commonly used.

There are catch-up deduction opportunities for manufacturers who may not have properly accounted for these costs, making it worth a closer look with your tax advisor.

Is Process Improvement Considered R&D?

When you think of research, you probably aren’t thinking of the life of a manufacturer. In actuality, the federal R&D tax credit under Section 41 was deliberately written to include the bread-and-butter work that Wisconsin manufacturers do every single day.

The legal standard isn’t “did you discover something new to the world?” It’s whether the activity was new to your company and involved a process of experimentation.

Do these activities sound familiar?

- Trying new approaches

- Evaluating results

- Refining processes

That’s the engineering floor of most mid-size manufacturers. So why are so many manufacturers not taking advantage of these credits?

Maybe you’ve heard of these credits, maybe not. If you didn’t before, now is the time to start paying attention. R&D credits for manufacturers are changing, and understanding the new laws is essential for securing a successful future.

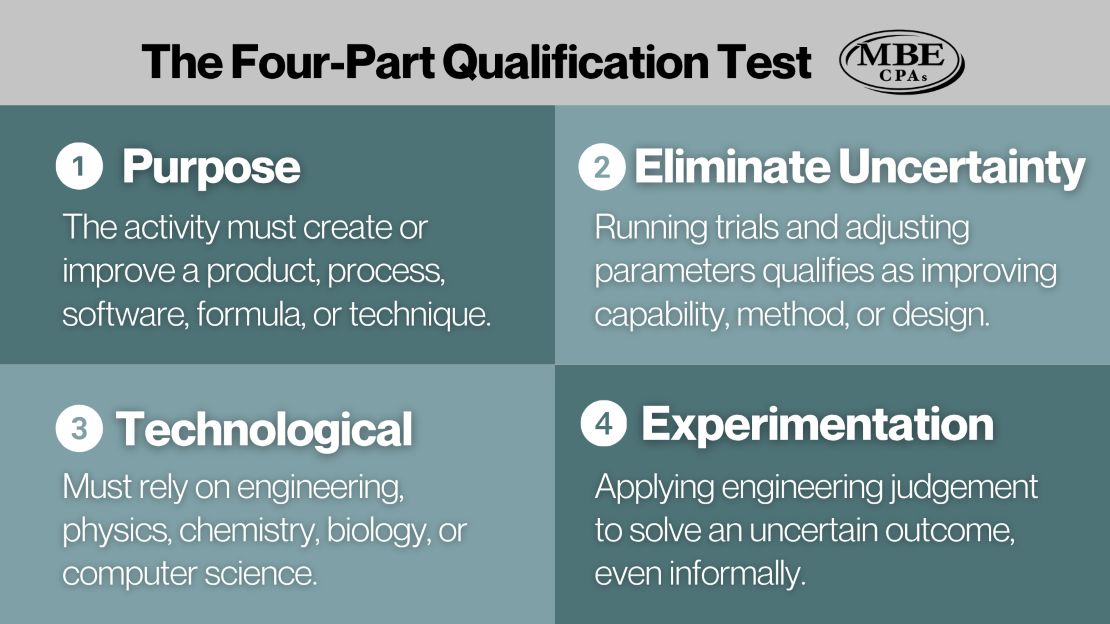

What is the Four-Part Qualification Test?

Most manufacturers have heard of R&D credits, but they fail to connect daily operations to the four-part qualification test. The IRS uses four criteria to determine whether an activity qualifies.

Here’s what they mean regarding the manufacturing floor:

- Purpose: The activity must create or improve a product, process, software, formula, or technique.

- Eliminate Uncertainty: Running trials and adjusting parameters qualifies as improving capability, method, or design.

- Technological: Must rely on engineering, physics, chemistry, biology, or computer science.

- Experimentation: Applying engineering judgement to solve an uncertain outcome, even informally.

The phrase “process of experimentation” is often misinterpreted. In manufacturing, to qualify for this, if your business applied a test, measured the result, and adjusted for a better outcome, that’s experimentation.

You don’t need a hypothesis, but it doesn’t count if you are just buying new equipment. Programming, integrating, and testing it does. It nothing was “uncertain,” then nothing was researched.

This distinction trips up many manufacturers:

- Purchasing capital equipment: Depreciation, bonus depreciation, Section 179

- R&D credit: The intellectual work of customizing that equipment to function in your production environment.

The keyword is custom. Implementing off-the-shelf software without modification is a hard argument for qualification. However, if your engineering team is writing production-specific code, then the credit attaches. Your actions must distinguish between routine and ordinary production.

Understand more about your business’s position.

The Frequently Missed Supply Chain Credit

Your team developed a new supplier qualification methodology, engineered changes to your inbound logistics, and created a proprietary system for managing traceability. You heard that R&D must occur in a lab, rather than on the factory floor or in logistics planning, so your team overlooked the credit qualifications.

Run the “technological in nature” test from the previous section. Here’s what qualifies:

- Using engineering analysis to redesign receiving and inspection processes

- Supplier qualification work tied to validating new material specifications

- Building a study for a new measurement approach

- Experimenting with how to improve storage, delivery, or scheduling processes

A pure procurement strategy doesn’t qualify on its own. But supply chain work that directly supports qualifying production development often does. The dividing line? Whether engineering analysis was applied to solve a technically uncertain problem. If that’s what your scenario looks like, then you’re closer than you’d think.

Structure your claims like these examples:

- “We documented three alternative approaches before selecting the current design.”

- “The engineer’s time was allocated to the new product line development project.”

- “We ran five different trials before identifying.”

Specificity wins, and vagueness invites disallowance. Even though these are strong examples, your accountant should be in the room. We study the credits your engineers might not yet be aware of.

What Documentation Should Manufacturers be Tracking?

Keeping detailed records of all qualifying research activities sounds reasonable. But your engineers are busy running a manufacturing operation.

The standard, tested through years of litigation, consists of three steps:

- Connect payroll record to specific qualifying activities

- Demonstrate that experimentation occurred

- Show the business component being developed or improved

The best documentation investment you can make costs almost nothing. You just need enough evidence for every engineering decision.

Here’s the documentation we suggest you start tracking:

- Project logs or engineering change orders: Most manufacturers already have these.

- Time tracking by project: Even rough allocations significantly strengthen a claim.

- Email threads on technical problems: Tracking why something isn’t working is contemporaneous documentation of experimentation.

- Test data, even informal: CMM reports, run charts, first-article data.

- Meeting notes from engineering reviews: Design reviews, FMEA sessions, tooling approval meetings.

- Drawing revisions with reason codes: Considered design alternatives and revisions.

Just by adding to your time-tracking system or training engineers to log project time, your clean time records will start paying for the credit study many times over.

How to Start Structuring Your Factory Floor

The most common obstacle is motivation and sticking to your plan. You know you qualify, but gaining the inertia to follow through is a different struggle. R&D credit studies feel like a big lift, so they stay on the someday list.

Here’s how to structure a defensible claim without pulling your engineering team off the floor:

- Project identification interview

- Payroll and time data pull

- Documentation gathering

- Credit calculation and review

When was the last time you evaluated the operational systems that underpin your business?

If you don’t know where to start, consider partnering with MBE CPAs. Our team does more than just accounting for manufacturers; we help strengthen every structural pillar of your manufacturing business.

R&D tax credits are particularly valuable when you’re making major equipment investments. If you’re purchasing automation equipment or production machinery in 2026, understanding depreciation timing can stack with your R&D credits for maximum benefit.