Do You Qualify for the Senior Deduction?

Authored by: Troy Hilyard — Partner, CPA | Date Published: March 5, 2026

If you’re 65 or older and live in Nebraska, there’s a good chance a new federal tax law is going to lower your tax bill without changing a single thing about how you live.

Congress quietly added a brand-new federal tax break for folks 65 and older. Here’s what it means in plain English, how much money you could keep in your pocket, and the one deadline you really cannot miss.

Key Points

- 300,000 Nebraska seniors are estimated to qualify

- $6,000: Maximum deduction for single filers age 65+

- $12,000: Maximum deduction for qualifying married couples

- 2028: The year the deduction is currently set to expire

What Exactly is the Senior Deduction?

Here’s the straightforward version:

The law in question, the One Big Beautiful Bill Act (OBBBA), created a new deduction specifically for taxpayers who are 65 or older. It’s deducted from your adjusted gross income (AGI), which means it reduces the pool of income that gets taxed before you even get to the standard deduction.

Here are the adjustments:

- Individual Above-the-line Deduction: Worth up to $6,000 per individual

- Partner Above-the-line Deduction: Worth up to $12,000 for married couples

These provisions start with the 2025 tax return you’ll file in early 2026.

Social Security remains taxable at the federal level, but what did change is that you now have a powerful deduction that wipes out a portion that would be owed on those benefits.

Think of it as Congress finally remembering that fixed-income retirees exist.

What’s the Good News for Nebraska Retirees?

Nebraska has already eliminated its state income tax on Social Security benefits as of 2025. Between the new federal deduction and the existing state exemption, many Nebraskans are looking at a dramatically lighter tax load this year.

For the average Nebraska retiree living primarily on Social Security, this deduction could eliminate federal income tax entirely. The average monthly benefit nationally runs just over $22,000 a year.

The important thing to note: Not every retiree will see their tax bill move.

Here’s the honest breakdown:

The senior deduction reduces taxable income, but it cannot create a refund if you didn’t owe any taxes in the first place. Think of it like a coupon that only applies when you’re actually buying something.

Let’s look at an example:

A widowed taxpayer receives over $20,000 a year in Social Security and takes $18,000 annually from their IRA. Under the old rules, roughly 85% of their Social Security income is taxable, bringing their AGI to around $35,000.

- With the standard deduction for a single filer, they owe federal income tax on around $18,000, which is about $2,000.

- Add the new $6,000 senior deduction, and their taxable number drops to $12,000. Now their federal tax bill could drop to the $600 range.

Not life-changing, but that’s at least a few months of groceries.

For more information about Nebraska’s tax changes, read more.

Nebraska’s SALT Cap Increase

Here’s the other OBBBA provision that’s flying under the radar in Nebraska. The SALT (State and Local Tax) deduction cap jumped from $10,000 to $40,000.

If you own a home valued at $300,000 in Omaha, you might be paying upward of $4,000 in property taxes already. Add Nebraska’s SALT taxes, and middle-income homeowners who itemize their deductions could see a meaningful bump from the expanded cap.

You might be asking, what’s the catch?

You must itemize deductions for SALT to matter. The expanded standard deductions still don’t apply to many seniors, but for those who do itemize, the new $40,000 SALT cap is real money.

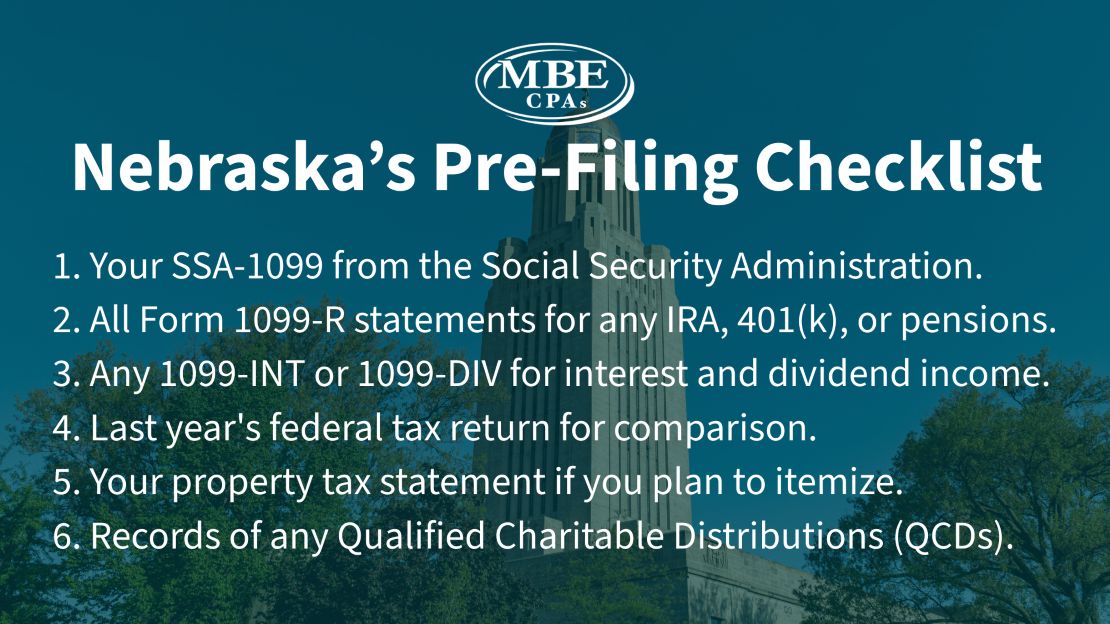

Your Pre-Filing Checklist

Before you sit down with your tax professional, here’s what to gather:

- Your SSA-1099 from the Social Security Administration.

- All Form 1099-R statements for any IRA, 401(k), or pension distributions.

- Any 1099-INT or 1099-DIV for interest and dividend income.

- Last year’s federal tax return for comparison.

- Your property tax statement if you plan to itemize.

- Records of any Qualified Charitable Distributions (QCDs).

The math matters, which is why pulling out your prior-year tax return and comparing the numbers is a worthwhile afternoon activity.

Common Questions from Retirees

Asking these questions now could save you hundreds or more. Even better: establish a partnership with a tax preparer.

For those quick questions that this blog might have brought up, we’ll provide you with answers.

Q: Do I need to do anything special to claim the senior deduction?

You’ll claim it on your 2025 federal income tax return. It’s a deduction applied to your AGI, and it’s not automatic unless someone does the math. Make sure your tax preparer knows you’re 65+.

Q: My income comes entirely from Social Security. Will this help me?

If you’re already paying no federal income tax, then no. The deduction can’t generate a refund on taxes you never owed. But it’s still worth checking, especially if any of your benefits were taxable under the previous law.

Q: Can I claim both the senior deduction AND the standard deduction?

Yes! The senior deduction reduces your AGI first, and then you can also take the standard or itemized deduction on top of that. For a single filer, stacking the deductions together can shield a meaningful chunk of your income from tax.

The 2026 tax filing season opened January 26. Don’t let the tax filing window close before you act. Working with an accountant becomes less about convenience and more about making sure you’re maximizing the savings you qualify for.

How an Accountant Can Help

Let’s bring all this together. What does this mean for you, practically speaking?

None of these breaks are complicated to claim, but they do require you to know they exist.

Does your tax return reflect it?

When you work with an accountant who understands Nebraska’s tax landscape, here’s what you’re actually getting:

- Income Stacking Analysis

- Itemize vs Standard Deduction Strategy

- Multi-Year Tax Planning

- Peace of Mind

Not all tax preparers are the same. If you’re going to work with a firm, look for a CPA with experience in retirement income planning, not just someone who does returns during tax season. Our team at MBE CPAs has strong familiarity with Nebraska-specific programs and how they interact with federal benefits.

Our team reaches out to you when laws change and models scenarios for you to consider before you make decisions. You can contact us from February through April, but we’re actually available to you year-round. As a partner should be.

If you’re 65 or older, live in Nebraska, and want someone to look at your specific situation, schedule a consultation with us.