You have built something most people only dream about. Signing your first franchise agreement was just the beginning, and now you are managing multiple locations, honoring development commitments, paying royalties, and growing a brand footprint that took years of hard work to build. With all of that income flowing through your partnership or S corporation, your tax bill at the personal level can hit harder than you expect, and that sting grows sharper with every location you add.

A state-level tax option called the pass-through entity tax (PTET) lets your franchise restaurant group pay state taxes directly from the business instead of passing that bill on to your personal tax return. To put this in context, let’s look at how this tax option works and what it may mean for your multi-unit franchise business.

What Is a Pass-Through Entity Elective Tax?

A pass-through entity elective tax is a state-level election that allows your business to pay state income taxes directly, rather than passing that tax burden down to each owner’s personal return. When your business pays state taxes, that payment becomes a deductible business expense on your federal return, reducing the income that flows through to you personally.

Unlike the standard state and local tax deduction on your personal return, which gets capped at the individual level, the PTET payment is treated as a business expense. Consequently, the payment is reported on the business return before the remaining items are distributed to your personal return, and it does so without the same federal cap that applies to personal deductions.

For franchise restaurant groups structured as partnerships, there’s an additional benefit worth understanding. When the business pays state income taxes through a PTET election, that payment lowers each partner’s share of self-employment income. State income taxes paid personally by partners don’t reduce their self-employment income, even when those taxes are tied to income earned through the business. For owners who pay self-employment taxes across multiple locations, this structural distinction directly affects how federal taxable income is calculated.

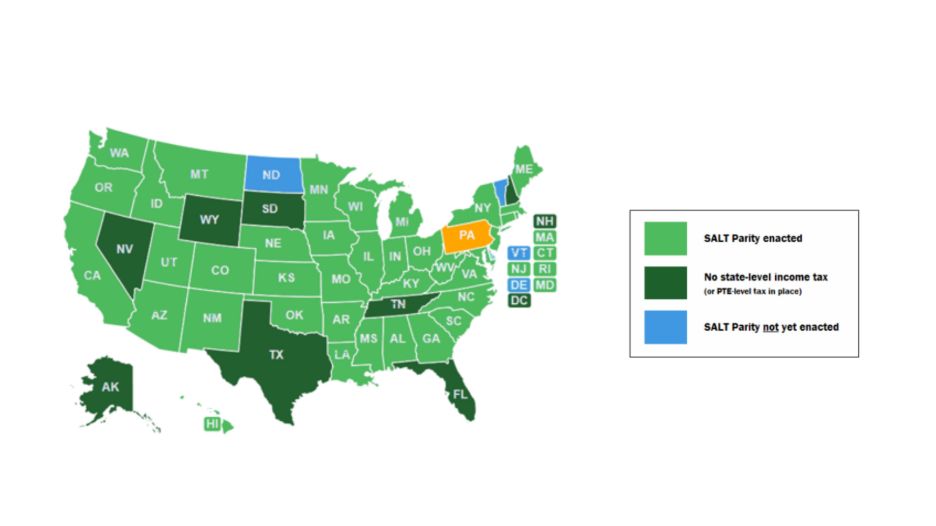

Which Restaurant Groups Qualify for the PTET Election?

Not every business structure qualifies, and understanding where your group fits is the first step. A significant number of states have a PTET program in place, and several more have proposed legislation to create one. Here’s how eligibility generally breaks down:

- Partnerships and LLCs taxed as partnerships: Multi-unit franchise groups structured this way are typically eligible in states that offer the PTET election, including multi-location restaurant groups where ownership is split between investors and operators.

- S corporations: Restaurant groups operating as S corporations are also generally eligible to make the election.

- Single-member LLCs: These are usually excluded unless the ownership has elected to be treated as an S corporation.

One important note on the election process: qualified businesses may elect to pay the pass-through entity tax if their owners hold more than 50% of ownership. Once made, the election generally cannot be revoked after the original due date. This means that getting your ownership group aligned early in the year matters, and it’s a conversation worth having before estimated payment deadlines.

What Does a Real-World Benefit Look Like?

I’ve worked with many restaurant owners to claim both SALT deductions and the PTET election, and the numbers can be significant. Consider a franchise restaurant group structured as a partnership that generates $1.2 million in net income across five locations. At a state income tax rate of roughly 5 to 7 percent, the state-level tax payment could be $60,000 to $84,000. The business records the payment as a deductible expense, reducing the federal income that flows to each owner, and owners then receive pass-through expenses in the form of tax credits on their state returns for their proportionate shares.

If a business paid $17,000 in state income tax personally and received no deduction because the personal SALT cap was already reached, paying that same amount through a PTET election from the business makes the full amount tax-deductible. For a multi-unit franchise group where owners have already reached the individual SALT cap, accounting for the payment at the entity level means the transaction is processed outside of the individual SALT cap restrictions.

Results will vary based on your income level, your other deductible expenses, and your state’s specific PTET rules and tax rates. Because these variables depend directly on your specific income level and corporate structure, a personalized review of your numbers is necessary before making the election.

What Do Multi-State Restaurant Operators Need to Know About PTET Rules?

Running locations across multiple states introduces real considerations into the PTET decision. As states continue to refine their programs, differences in election procedures and credit structures make it important to revisit the decision annually. Here are the key areas to stay on top of:

- Election deadlines vary widely by state. Some states require the election as early as March 15, while others allow elections through the extended return due date. Missing a deadline typically means losing the election for that year entirely.

- Quarterly estimated payments are generally required. Most states require estimated PTET payments throughout the year, so your cash flow planning should account for these in advance.

- Owner residency determines how the tax credits are allocated. Some states calculate the PTET differently for resident versus nonresident owners, which changes how much credit each person receives on their personal return.

- State legislation keeps moving. Some states have made their PTET programs permanent, removing uncertainty for long-term planning. Others have extended election deadlines, giving groups more time to make informed decisions with more complete financial data. States including Colorado, Wisconsin, Arizona, and Nebraska, where our team at MBE CPAs regularly works with franchise restaurant clients, each have their own rules, timelines, and credit structures that deserve attention.

Because state tax regulations change, multi-unit operators must routinely monitor legislative updates to remain compliant. Laws change, deadlines shift, and a missed update can cost your group the election for an entire tax year. Coordinating with a CPA who monitors multi-state tax updates helps sync your deadlines and credit structures across your entire footprint.

Is the PTET Election a Good Fit for Your Restaurant Group?

The pass-through entity tax election is not a one-size-fits-all decision, nor a set-it-and-forget-it strategy. It needs to be weighed against your group’s ownership structure, the states where you operate, and your personal tax picture each year.

One piece that often gets overlooked is the timing of estimated payments. Your business pays those state taxes throughout the year in quarterly installments, which means your operating accounts need to support that payment schedule. For groups with predictable income and stable profit margins across locations, this is often very manageable with the right planning. For groups with more seasonal or variable income, the timing of those payments deserves careful modeling before committing to the election.

If your group hasn’t taken a close look at the PTET election, or if you operate in multiple states and aren’t sure how the rules apply in each, our team at MBE CPAs can walk through the considerations with you. We’re happy to sit down, review your numbers, and help you determine whether this election makes sense for your restaurant group.