Most manufacturers can tell you their top-line revenue, their direct labor cost, and their material spend down to the cent. What they often can’t tell you is whether their overhead allocation method is silently mislabeling profitable products.

How confident are you that you aren’t subsidizing the costliest products at the expense of everything else?

What Is Overhead Allocation and Why Does It Matter?

Somewhere underneath your growing revenue and busy plant floor, your margins are quietly compressing.

Overhead allocation is the process of systematically distributing indirect manufacturing costs across your products.

Here’s a look at those costs that aren’t tied to a single unit:

- Rent on the plant floor

- Depreciation on equipment

- Supervisory salaries

- Utilities & maintenance

- Quality control labor

- Insurance

While they don’t exist in isolation, they’re all required to manufacture anything, and they typically represent 20% to 40% of your total manufacturing costs. Spread overhead wrong, and your pricing, product mix, and investment decisions are based on inaccurate numbers.

- Product costing: What you believe it costs to make each unit

- Pricing: Whether your quotes cover your real costs

- Product mix: Which product lines you should invest in

- Inventory valuation: What shows up on your balance sheet and COGS

Now, how do you allocate them?

What Common Allocation Mistakes Do Manufacturers Make?

Assigning your overhead incorrectly will distort the foundation of all four of those downstream decisions. You might overprice your most competitive product or expand a product line with a secretly horrifying cost structure.

Avoid these six mistakes that manufacturers make when distributing their overhead:

- Using a single rate across departments: A single rate makes sense if overhead is consistent across every department. But machine processes consume overhead differently than hands-on, and grouping them under a single rate blurs that distinction.

Establish departmental overhead rates, or separate rates for machine-intensive and labor-intensive production areas.

- Treating all labor hours as equivalent: The overhead difference between a machinist’s operation and a technician’s hand-finished part is huge. Maintenance, depreciation, and energy are tied to machine time, not headcount. Subsidizing hand labor begins when your rate is based on direct labor hours.

- Setting the rate and not revisiting: Many manufacturers set their rate at the beginning of the year, forgetting that predetermined overhead rates are estimates. When actual production diverges from those projections, being charged too much or too little will, regardless, distort your product costs and your inventory valuation.

Watch for consistent end-of-year finishes with large overhead variances to determine if your rate is structurally off.

- Ignoring setup and changeover costs: Under a volume-based allocation, long-run products absorb most of your setup costs just from producing more units. This makes short-run, high-changeover products appear more profitable than they are.

Make sure the orders you accept are priced accurately based on the true cost of accommodating them.

- Excluding quality costs: When your plant runs standard products alongside complex components, it’s important that rework labor and quality inspection aren’t treated as a flat overhead line item. When the rate difference isn’t captured in your costing, you’re essentially passing the cost of complexity on to your standard product customers.

Quality doesn’t come free. Understand the true cost.

- Relying on nonexistent capacity: Real costs aren’t being recovered through product pricing when a plant runs at half capacity but calculates its rate based on 90% utilization. This drags margins, but is hard to identify because the rate always looked reasonable on paper.

The deceptive thing about inaccurate overhead allotting is that it isn’t dramatic enough to trigger a crisis. Your cost system hasn’t improved because you’re blaming shifting margins on the market or competitive pressure.

If you’re questioning whether your costing system is right for your operations, learn more about how to identify the true drivers of your expenses.

How Can You Fix Your Overhead Allocation?

You don’t have to implement a full activity-based costing system to improve your overhead. ABC is powerful, but it’s also resource-intensive to build and maintain.

Improvement can start with a few targeted changes.

- Map your overhead: Identify major categories of overhead cost and ask simple questions for each, like what drives this cost? Begin to see whether a single base is capturing this behavior.

- Move to departmental rates: Split your plant into cost pools and assign a separate rate to each to improve costing accuracy.

- Review rates regularly: Compare your predetermined rates against actual overhead costs to understand why the volume was lower than expected or if overhead costs spiked in a specific area.

- Separate setup and changeover costs: Pull costs out of general overhead pools and assign them based on setup events or hours.

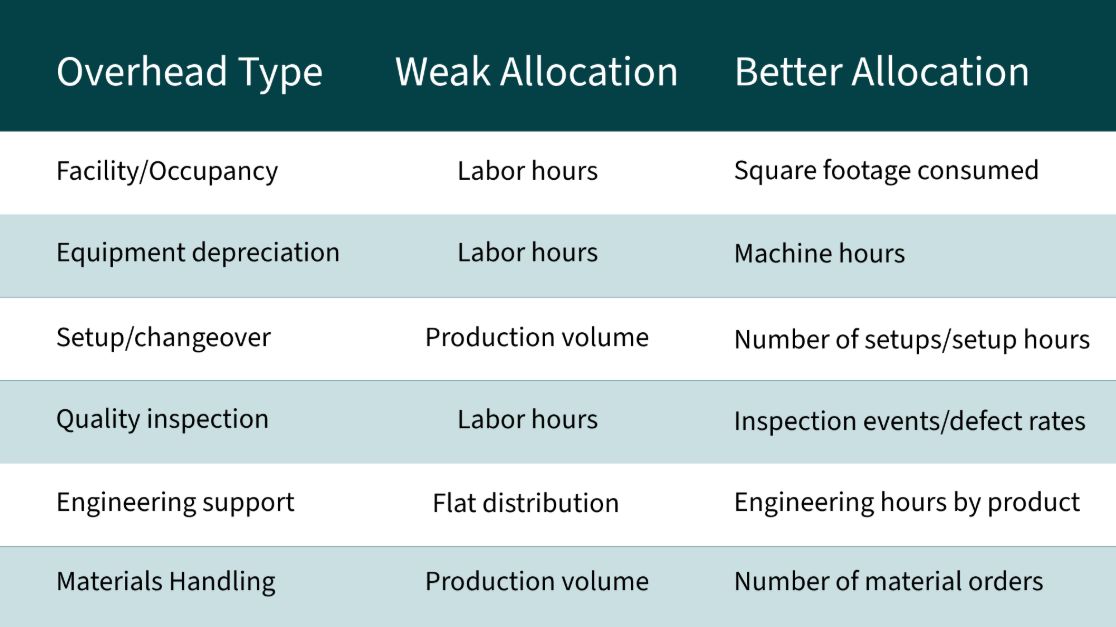

Here’s how certain overhead types should be assigned:

What does this look like in the real world?

A mid-size manufacturer producing both commodity components and specialty parts has been using a plant-wide overhead rate based on direct labor hours for years. The owner’s intuition says the specialty parts business is the real profit engine. Margins look better, customers are loyal, and they’re willing to pay.

The picture reverses when the overhead is properly traced, showing that specialty parts are running below what the labor-hour rate was reporting.

The owner had been considering investing in additional capacity. That decision, based on the old numbers, would have shifted money from true profits to the loss driver.

Allocating your costs may not seem as important as it really is until you realize you’ve been losing money for years. It’s the kind of structural analysis that changes how you see your own business and occasionally reverses decisions that once seemed obvious.

Explore the adjacent cost decisions that compound the impact of getting overhead right.

When to Outsource Your Overhead Questions

Your intuition is built around the numbers you have, and questioning whether those numbers are accurate requires stepping back. This is easier said than done when you’re busy running a plant. That’s what we often see: the people closest to the numbers are often the least positioned to spot them.

If your costing system has been operating a certain way for years, its output starts to look like the truth rather than estimates. It’s important you don’t get the two confused.

Let’s look at situations where outside accounting tends to be valuable.

- You see overall margin compression despite stable raw material costs and no pricing changes.

- Your most complex products appear to be your most profitable.

- You’re evaluating a significant capital investment tied to a specific product line.

- You’ve expanded your product portfolio significantly and haven’t revisited your costing method.

- You’re considering removing a product line or customer relationship based on margin data.

The decision you make is only as good as the data underneath it. Proper overhead analysis examines not just the rate but also the cost pools driving it, the allocation bases chosen, the capacity assumptions, and the variance patterns that emerge at the end of the period.

When you feel like your overhead distribution is working against you, consider partnering with experienced advisors. Our team at MBE CPAs works with manufacturers to surface the costing blind spots that compress margins over time.

We understand the challenges that manufacturers face, and we are here to help you succeed.