Globalized manufacturing enters a new era

ARTICLE | January 10, 2023

Authored by RSM US LLP

The era of globalization, which brought cheap goods, low inflation, rapid growth and inexpensive capital, is transitioning to a new state. Globalization is not dead, but the makeup of its participants has shifted, and global trade rules continue to be rewritten as businesses diversify where they source and make their goods. The impact of these structural changes is profound.

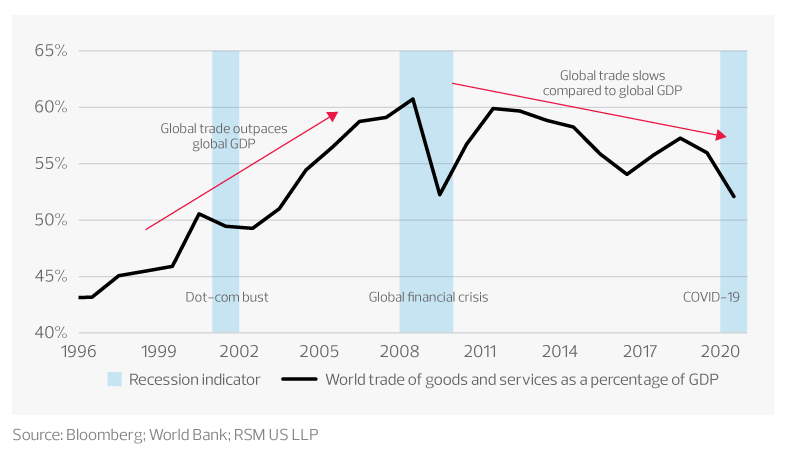

This isn’t a new narrative; world trade as a percentage of world gross domestic product has been on a downward slope since the global financial crisis. But strained government relations and new policies have pushed manufacturing further into this new era. As a result, industrial companies will need to assess alternative strategies and operational locations.

Middle market insight

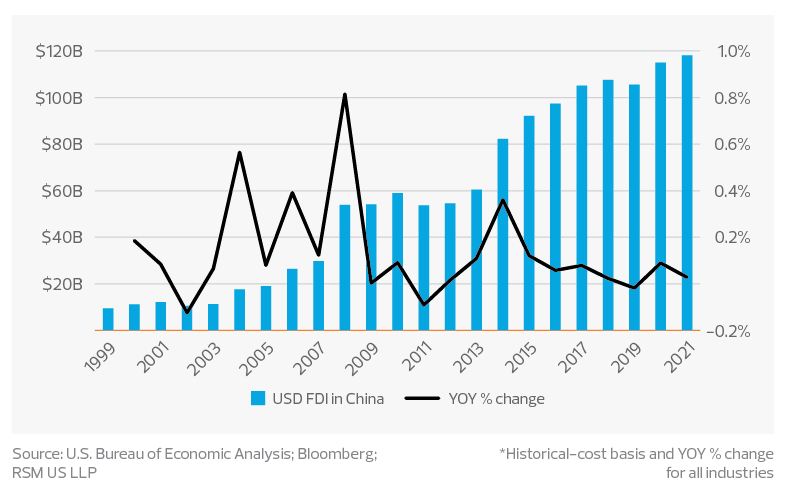

Since 2016, the year-over-year percentage change of new U.S. foreign direct investment in China consistently slowed to single digits—signaling a more tepid investment appetite.

Trading with unfriendly nations like Russia is taboo. Trade with China in certain technologies related to telecom, computer chips and surveillance is verboten. The number of businesses and people on the U.S. Commerce Department’s restricted entity list doubled to nearly 1,200 between 1997 and 2000, and the world put 9,098 new sanctions on Russia since the start of the invasion of Ukraine. The saber rattling with China, plus another term with the current Chinese leadership, is leaving businesses wary of further investment in the country.

World trade of goods and services as a percentage of GDP chart

Of course, global trade wasn’t always this way. The world embraced its last surge in global trade when the Berlin Wall fell in 1989. Global trade became policy. In 1995, the World Trade Organization was founded to reduce tariffs and make trade smooth, predictable and free. Then China joined the WTO in 2001, codifying its shift as the factory of the world, and the United States led support for that shift by investing over $118 billion in China by 2021. U.S. living standards rose, as did a global middle class through access to lower-priced, easy-flowing goods and job creation. Growth was high, and inflation stayed low.

But all of this has changed. Since 2016, the year-over-year percentage change of new U.S. foreign direct investment in China has consistently slowed to single digits—signaling a more tepid investment appetite.

U.S. foreign direct investment in China* graph

Starting in 2018, the United States slapped tariffs on Chinese goods, and a trade war began. Then in early 2020, the pandemic sent shock waves through global supply and demand. Two years later, war broke out in Europe and exacerbated inflation through the energy and commodity channels. Geopolitical tensions reset to Cold War levels.

Individually, these events weren’t tipping points, but their cumulative shocks echoed throughout policymaking bodies and boardrooms worldwide, leaving an indelible mark on the global economy.

New math, new incentives, different options

The total historical cost of U.S. foreign direct investment in China of $118 billion is slanted heavily to the manufacturing sector, with 48.2% (or $56 billion) going to food, chemicals, metals, machinery, computers, electrical equipment, transportation and other sectors. After that, wholesale trade is the largest nonmanufacturing sector and represents 15.5% or $18.3 billion of U.S. investment. These sectors represent the core investments in China that make and move goods, and rapid change in these areas is difficult.

Middle market insight

A mix of legislative incentives and deterrents is helping create a?U.S. renaissance?in manufacturing for semiconductors, telecom materials and 5G infrastructure.

Now calculations made 15 to 25 years ago about where to source and manufacture goods are outweighed by security interests, increased risk, productivity losses, higher costs and uncertainty.

A recent mix of legislative incentives and deterrents is creating an about-face and helping create a U.S. renaissance in manufacturing for semiconductors, telecom materials and 5G infrastructure. Other incentivized U.S. investment priority areas include green energy equipment, active pharmaceutical ingredients, and strategic and critical minerals.

In August 2022, legislators signed the CHIPS and Science Act into law, directing $200 billion in spending on research and development and over $52 billion on semiconductor manufacturing over the next 10 years.

That same month, the Inflation Reduction Act was codified into law and will invest $369 billion in energy security and climate change programs over 10 years.

This leaves a multitude of other consumer goods and industrial manufacturers that invested in China assessing alternative strategies. It is unrealistic to believe many of these businesses will return to the United States.

Barring immediate strategic needs or government incentives, locations for such operations will continue to depend on labor, access to materials, transport costs, proximity to end customers, and risk profile.

For businesses that explore alternatives, the key options are to continue to invest in China and do business as usual, curtail new investments in China but maintain operations there, or close operations there and relocate within the Asia-Pacific region or near-shore to a country like Mexico.

Whatever route companies take, they won’t be able to ignore China’s market. It is the United States’ largest goods and services trading partner, and future market access is important. Additional U.S. investment in China is likely to continue its taper compared to prior periods in favor of other markets like India or Mexico. Still, the extent of that slowing investment remains to be seen.

How should businesses adapt?

Manufacturers need to consider a host of internal and external factors when deciding whether to explore alternative locations. The weight of each factor will vary by business.

Internal factors include whether the organization has the management capacity and experience to develop a new manufacturing strategy. This effort requires taking the time to research options, as well as seeking input from team members and stakeholders, calculating the financial and nonfinancial impacts, evaluating risk, and creating an investment schedule and road map for decision-makers.

Middle market insight

Businesses that diversify their manufacturing footprint should use the opportunity to ask themselves what they can do better.

External factors include transportation and logistics costs and options, labor, material sourcing, customer proximity, ease of operating, technological requirements, cost of capital, tariffs, taxes, regulatory requirements and, of course, geopolitical risk.

Projects like these are disruptive for many of today’s lean management teams. The substantial level of effort and potential capital investment involved will deter some businesses from changing where they operate. But given the shifts in globalization, businesses need to thoroughly examine whether diversifying their locations will maximize their long-run prospects.

Change equals opportunity

Businesses that diversify their manufacturing footprint should use the opportunity to ask themselves what they can do better. Answering this question can unlock unexpected enterprise value.

Adopting new productivity-enhancing equipment and state-of-the-art technology, for instance, can reduce reliance on labor, lower variable costs and maximize long-term capital investments.

A way to explore these options before making costly decisions is by using digital twin technology to create 3D models of shop floors, equipment layouts, and employee productivity and run myriad scenarios to identify the most efficient use cases.

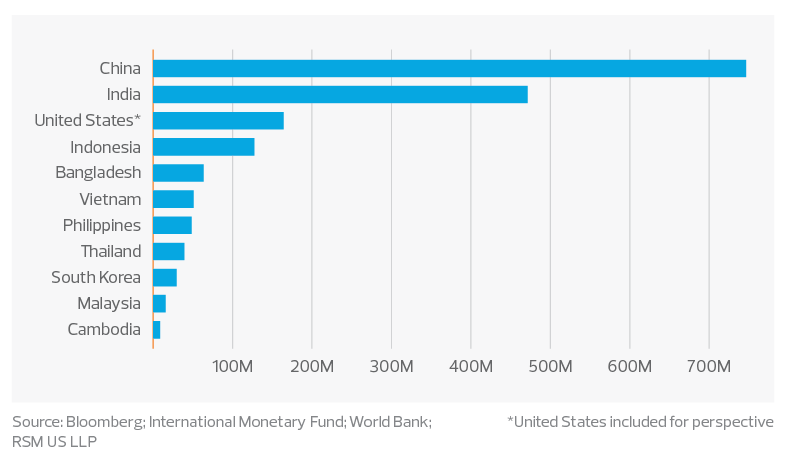

Solving for access to talent and labor, no matter the country, will present challenges compared to China; no country except India will match the size of its workforce. Augmenting labor and automating tasks will be necessary for scenarios where labor costs are higher and access to workers more limited.

Labor force totals by country—Asia-Pacific region 2022 graph

The takeaway

Whatever the mix of key driving factors for each business, manufacturers that reassess what this new global picture means for their operations can likely find efficiencies in terms of transportation costs, energy or raw materials. Operating in new locations can create different tariff opportunities, transportation savings and landed cost savings.

This article was written by Matt Dollard and originally appeared on Jan 10, 2023.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/industries/manufacturing/globalized-manufacturing-enters-a-new-era.html

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each are separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/aboutus for more information regarding RSM US LLP and RSM International. The RSM(tm) brandmark is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

MBE CPAs is a proud member of RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise, and technical resources.

For more information on how the MBE CPAs can assist you, please call us at (608) 356-7733.